The issue of debt repayment today is quite relevant and is widely discussed in legal circles. In particular , one of the most discussed is the issue of the possibility of writing off debts by the statute of limitations . Debt cancellation is often the best option for both parties to the agreement - for the creditor and the debtor. However, both parties need to correctly display the fact of write-off in the reporting and follow its procedure.

The concept of arrears

Overdue accounts payable - these are funds that were received by the debtor from the creditor on the basis of various kinds of agreements and were not returned within the period established by the terms of the transaction. Traditionally, such agreements are a loan agreement and a loan agreement (in combination with methods of securing the fulfillment of an obligation or without them). The basis for the occurrence of debt (overdue) is two main legal facts:

- Conclusion of an agreement between the parties, providing receipt of funds by one of the counterparties.

- Failure to return the funds received by the party within the period established by the terms of the transaction.

After the term for the return of funds has expired, the counterparty under the contract, which has not fulfilled its conditions, acquires the status of a debtor. From this moment on, the parties to the contractual relationship are called " debtor"And" creditor». After determining the presence of debt, the creditor receives a fairly large number of rights. All of them relate to the return of funds transferred legally, as well as obtaining additional "compensation" for non-fulfillment of the contract by the counterparty. Such "compensations" include interest on the use of the loan and penalties for non-compliance with the terms of the transaction. For some types of contract, creditors (especially secondary creditors - persons who have acquired the right to claim under a factoring contract ( assignment of the right to claim) also charge additional commissions for servicing the contract.

For the lender debt has a double meaning. First, she is undoubted loss. In this case, the logic is quite simple - the funds were given, but were not returned. Secondly , it can be included in income. At taxation, for the creditor this fact plays an important role. However, in order for the definition of overdue debts as income to be carried out correctly, the creditor needs to know how to write off accounts payable.

Deadline for writing off accounts payable

The determining factor for identifying the write-off possibility is the statute of limitations for the write-off of accounts payable. Its calculation is repelled from another basic term in civil law - the statute of limitations. The general statute of limitations is 3 years. The beginning of the deduction of this time period occurs from the moment when the person learned or presumably could learn about the violation of their rights. For credit legal relations, such a moment is the debtor's "delay". That is, it is from the moment of failure to make the first payment under the loan agreement in accordance with the established schedule that the limitation period should be counted, and, accordingly, the period for writing off the debt.

In legal circles, there are often discussions on the subject of the start of the countdown of the limitation period and debt cancellation. Some experts believe that the limitation period for credit agreements and loan agreements should begin from the moment the agreement expires specified in it. However, judicial practice almost unequivocally accepts the position of the moment of delay as a starting point. After the expiration of the time period of 3 years, the creditor is entitled to write-off.

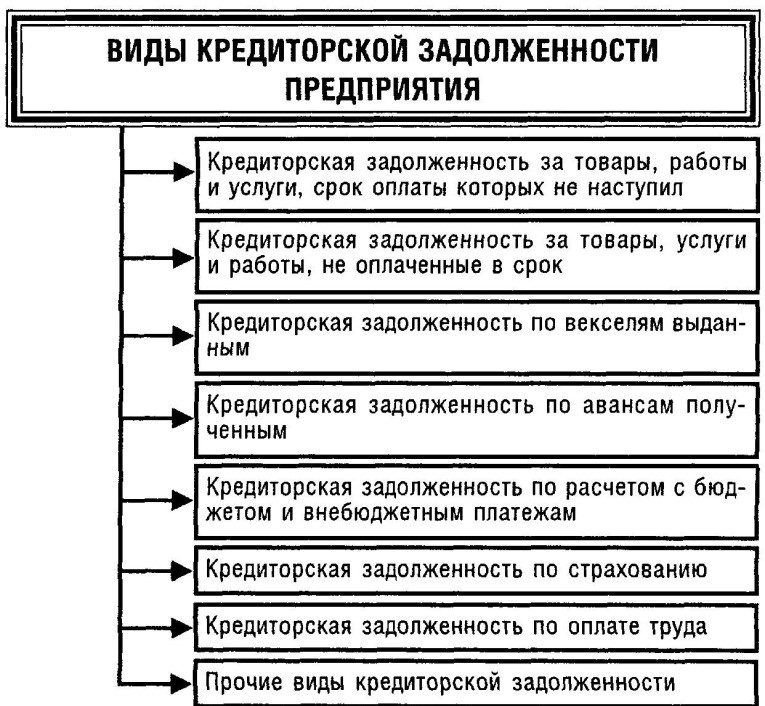

Types of accounts payable

When calculating the term, you need to remember about the possibility of interrupting it. According to the general rule, the limitation period is considered interrupted if the debtor has carried out certain actions, testifying about recognizing their debt. Such actions include:

- written recognition of the claim;

- recognition of the claim in part (for example, in part of the "body" of the loan or interest) and the denial of the claim in another part;

- signing the act of reconciliation;

- conclusion of the contract restructuring debt;

- liquidation of a legal entity-debtor;

- death of an individual debtor;

- partial payment under the contract .

If one of these actions took place: the limitation period is interrupted and starts its countdown anew, and accordingly, the period for recognizing the debt as overdue is interrupted.

Also, civil law establishes the possibility of stopping the limitation period. Such a stop is provided in cases of service of a citizen in the ranks of the Armed Forces, illness, etc. When the limitation period is stopped, its countdown after the elimination of the circumstance - the grounds continues (and does not start anew, as happens during interruption). In case of interruption of the limitation period, the calculation of the period for writing off the debt begins only after the circumstance that became the basis for the interruption has been eliminated. For example, an individual - the debtor returned from the army - the period continues to count down from this moment.

Write-off of accounts payable

The procedure for writing off debt requires clarification from the point of view of its formal display. In order for the write-off to be considered carried out in accordance with the established procedure, the creditor must draw up the following documents:

- order (order) of the head of the creditor organization;

- inventory act.

The inventory act must also be supplemented by a clear description of the assets that directly are related to the amount of debt. Formally, such an amount of debt is displayed in the category " Other income" (" Other income"). The transfer of monetary amounts to the category of other income is possible only if the debt is recognized as uncollectible. To recognize a debt as such, it is not necessary to issue a specific act or any other document. Sufficient is the statement of the fact of the expiration of the limitation period under the contract.

Also, the basis for writing off accounts payable is the impossibility of fulfilling the obligation for objective reasons. In order to avoid manipulations with the concept of "objective reason", the legislator has established a list of such reasons. These include :

- the presence of an act of the body state power;

- the unreality of debt collection according to the creditor's own assessment.

In practice, under the act of the body state power means an act executive bailiff about the end executive production and the impossibility of collecting debt from the debtor. In accordance with the Decree YOU from 07.08.2008, for purposes taxation such a basis may be considered legitimate.

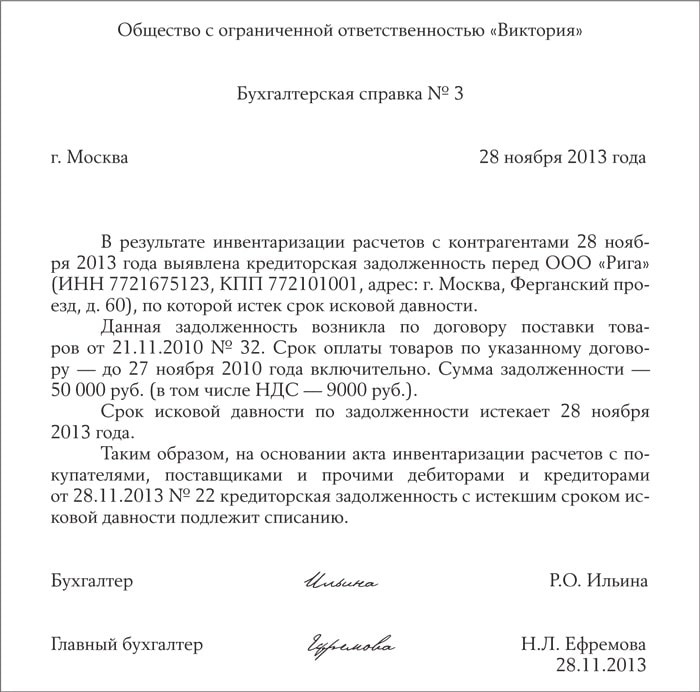

Sample accounting statement on write-off of accounts payable

Another criterion is the assessment of the creditor organization itself, which is rather vaguely displayed in legislation. At first glance, it is enough for a creditor to evaluate and substantiate in writing the impossibility of debt collection, but in practice it is not enough to substantiate the impossibility of such collection. Subsequent debt relief only raises questions about expediency and the legality of such actions by the tax inspectorate. If such actions were carried out after the expiration of the limitation period, debt write-offs are considered quite logical. However, before this deadline, it must be well justified.

Tax accounting when writing off

For purposes taxation writing off overdue accounts payable is of paramount importance in the context of two main taxes:

- VAT;

- income tax.

Some financiers mistakenly believe that if the debt is written off, there is a possibility of VAT recovery. Tax Code of the Russian Federation provides closed list of VAT recovery cases, previously granted to the deduction. There is no case of debt write - off in this list , so VAT recovery on such a basis is groundless .

As for income tax, here the debt is of great importance for the accounting of the debtor's profit. If creditor on throughout term claim prescription (3 of the year) Not declared O their requirements concerning return monetary funds By conditions deals, debtor must such monetary facilities display V his reporting How non-operating income. At this such non-operating income must be displayed With taking into account VAT.

Necessary Mark, What write-off debt, By which expired term presentation requirements , at all Not means cancellation such debt . After holding procedures write-offs, V established law okay debt displayed V accounting reporting on throughout five years.

Is being done This For Togo, to, V case changes material provisions debtor And appearance at him possibilities return duty, creditor revealed this fact And tried debt recover.

Education debt between contractors By treaty is one from most simple V legal respect And most widespread institutions civil rights (which more Right will name conflict situations V legal field). That's why enough exact his settlement is one from major tasks civil law enforcement practices.