Part of the costs of dental treatment, replantation, implantation, installation of metal structures and other dental procedures, the legislator allows you to return through a social tax deduction. One of the main conditions is a correctly compiled package of documents submitted to the Inspectorate at the place of registration of the person. The maximum amount of the deduction is 120 thousand rubles, for expensive medical services, expenses are accepted in full.

The Tax Code of the Russian Federation provides for the possibility of returning part of the funds spent by a person for treatment, education, charity, etc. This tax preference is called a social deduction.

The most frequently claimed right to reimbursement of costs associated with treatment is dental services: dental prosthetics, implants, bridges, etc. One of the main conditions for obtaining benefits is the preparation and submission to the Inspectorate of a package of documents for a tax deduction for dental treatment. In addition, there are a number of other requirements, without which it will not be possible to reimburse the costs.

Grounds for deduction

- Receipt in the year in which the treatment was made, income at a rate of 13%.

If income was received in the specified period, for example, at rates of 9% and 35%, then it will not be possible to reimburse expenses. This is due to the fact that the basis of the social deduction (SC) is a reduction in taxable income at a rate of 13%, and not a simple reimbursement for medical services.

- Inclusion of performed dental procedures in a special list approved by the Decree of the Government of the Russian Federation.

In accordance with this list, the costs of replantation, implantation, installation of metal structures are classified as expensive types of treatment, the SV for which can be received in the amount of the full cost of the funds spent.

With regard to the installation of dentures, the financial department in its letter dated December 25, 2006 (Appendix No. 1) indicated that dentures are not included in the list of expensive services and costs for it can be accepted in the amount of no more than 120 thousand rubles.

However, in the same document, the Federal Tax Service noted that the Ministry of Health and Social Development was vested with the authority to classify certain medical manipulations as expensive.

The Ministry of Health and Social Development, in its letter, classified denture implantation services as an expensive type of treatment:

It should be noted that if code 1 (regular service) and not 2 (expensive) is indicated in the certificate issued by the medical organization, then the SV will be charged only for expenses not exceeding 120 thousand. If such a situation occurs, you can ask the employees of the institution to correct the code , motivating this by the fact that the treatment is classified by the Ministry of Health and Social Development as expensive. But a person is not entitled to demand a change in the indicator, since the decision to classify certain services as expensive is at the discretion of the medical institution.

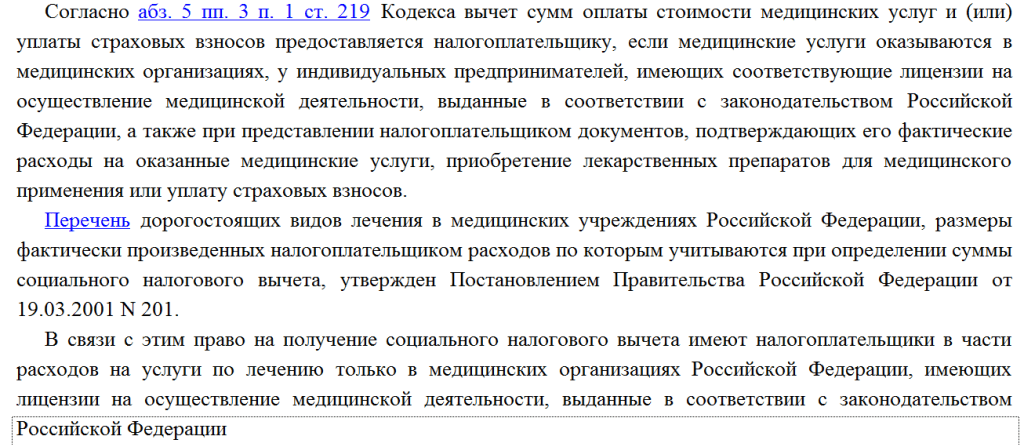

- A dental organization or individual entrepreneur who provided services must have a license to carry out medical activities.

You can check whether a clinic or individual entrepreneur has the necessary license on the website of Roszdravnadzor.

- Treatment must be carried out on the territory of the Russian Federation

It will not be possible to receive a tax deduction for the treatment and prosthetics of teeth abroad. This is directly stated in the following letter from the Ministry of Finance of the Russian Federation:

The amount of the deduction and its transfer to subsequent periods

Unused balance cannot be carried over to the next year (Appendix 2).

The right to refund income tax for dental treatment can be exercised within 3 years from the date of the costs incurred.

How to get a tax deduction for dental treatment for relatives

You can reduce the personal income tax base not only for expenses for yourself, but also for your immediate family.

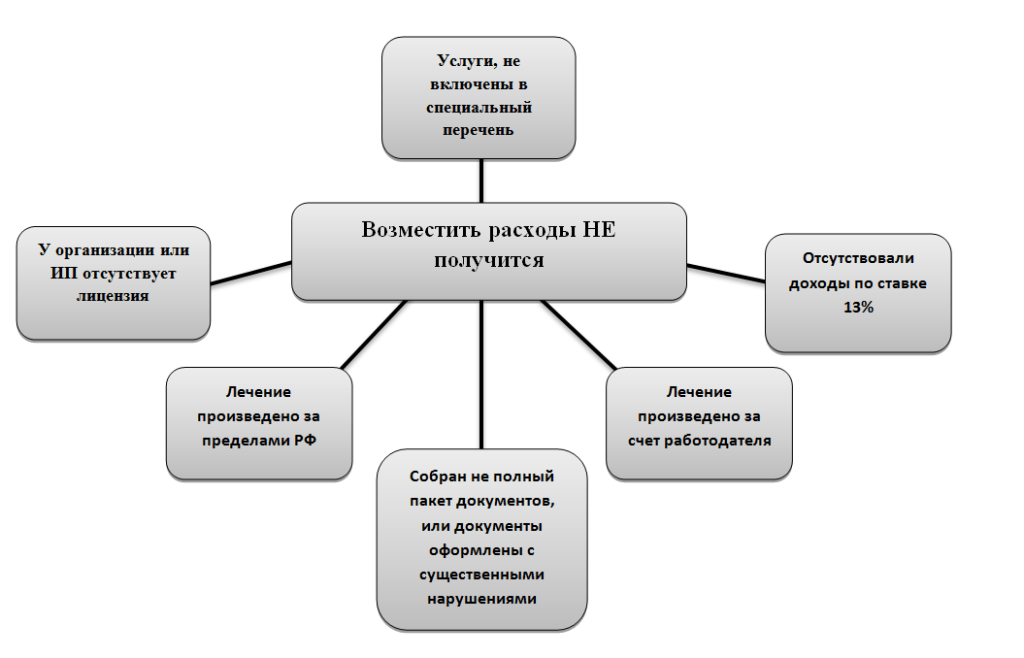

In what cases will a refund be refused?

Required documents for deduction and features of their completion

The standard package of documents submitted to the Inspectorate includes:

This list is established by the Letter of the Finance Department and is exhaustive. The Inspectorate is not entitled to refuse to return personal income tax for failure to submit checks, licenses or other documents not named in the list.

In order to exclude the claims of the Inspectorate employees, we still recommend attaching the following documents:

- Copy of passport and TIN;

- Copy of the license;

- Checks for payment of dental services;

- Help 2-NDFL

The main stages of registration

- Collect the necessary package of documents;

- Fill out the declaration;

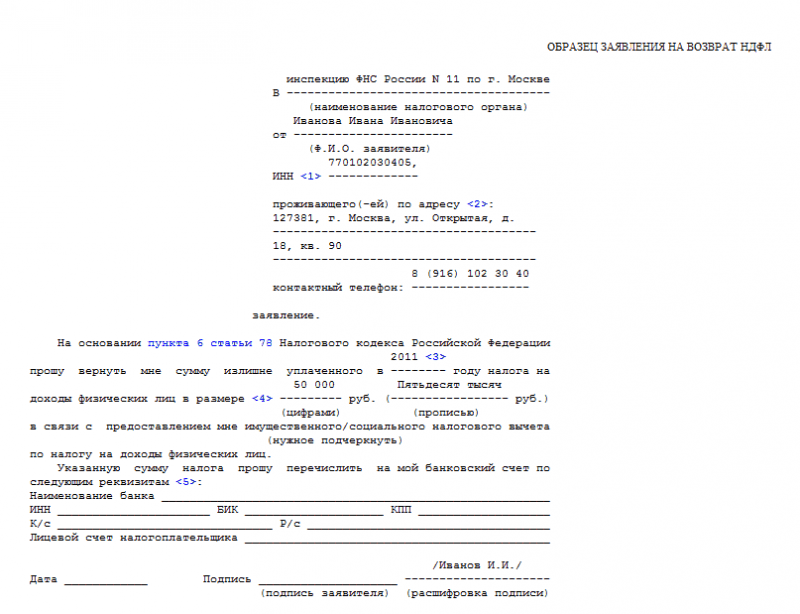

- Submit documents in person, by mail or through a representative to the Inspectorate at the place of residence (refer to clause 4 of article 80)

If the FL acts through a representative, then he must have a notarized power of attorney to represent interests.

- Wait for the decision of the tax authority

Within three months from the date of receipt of the documents by the Inspectorate, a desk tax audit (CIT) is carried out, as a result of which a decision is made to return or refuse to return personal income tax.

In case of a positive result, the funds must be transferred within a month from the end of the CNI.

If the application submitted together with the declaration did not specify the details to which the funds must be transferred, or it was not attached at all, then the tax refund will be made only after the specified document is submitted to the Inspectorate. The return period will be one month from the date of receipt by the tax authority of an application with bank details.

If, based on the results of the KNP, the deduction is denied, then the FL may appeal against the specified decision to the Inspectorate that conducted the audit, to a higher tax authority and to the court.

It should be noted that filing a claim with the court is possible only if the pre-trial procedure for appeal is observed.

Calculation procedure

The calculation of personal income tax to be reimbursed for services that are not related to expensive services is made according to the following formula:

The amount to be reimbursed from the budget is calculated taking into account the income paid in the tax period. That is, you can return the tax only in the amount in which the personal income tax was paid to the budget.

Example #2

FL in 2015 carried out implantation and dental prosthetics in the amount of 500 thousand rubles.

Since dental prosthetics is classified as an expensive service, the costs of it are subject to reimbursement in full.

The maximum deduction that can be claimed is 65 thousand rubles. (500 thousand * 13/100).

According to the 2-NDFL certificate, a person's income in 2015 amounted to 480 thousand rubles, personal income tax paid to the budget - 62,400 rubles. (480 thousand * 13/100).

A person can reimburse personal income tax from the budget in the amount of 62,400 rubles. At the same time, the balance is 2,600 rubles. cannot be carried over to the next year.

Example #3

In 2014 Alekserov V.V. paid for the installation of implants in the amount of 800 thousand rubles. for his wife, braces for his daughter (15 years old) in the amount of 100 thousand rubles. and dental prosthetics for himself for 150 thousand. The costs amounted to 1,050,000 rubles. The maximum amount of SV can be - 136,500 rubles.

Income of Alekserov V.V. in 2014 amounted to 2.5 million rubles. The amount of personal income tax calculated and paid to the budget for this income is 325 thousand rubles. Accordingly, he will be able to declare and reimburse all costs in the amount of 136,500 rubles.

Features of filling out a declaration

- The document can be filled out both by hand and using special programs;

- Ink color allowed blue and black;

- Corrections, printing on both sides, damage to the barcode and loss of other information due to inaccurate binding of sheets is not allowed;

The following sheets and sections must be filled in the declaration:

- Title

- Sections 1 and 2;

- Sheet A and E

For more information on how to fill out the declaration, see the following video:

Innovations 2016

According to the amendments made to the Tax Code of the Russian Federation and coming into force on January 1, 2016, a person can claim a deduction not only through the tax authority, but also at the place of work before the expiration of the year in which the expenses were incurred. That is, if the treatment was paid for in 2016, then the costs will be reimbursed in the same period.

It will be possible to reduce personal income tax by submitting an application and a certificate confirming the right to a deduction (to receive it, it will be necessary to submit a package of documents to the Inspectorate and within 30 days the tax authority must issue the specified document).

This procedure will be applicable from January 01, 2016.

Summarizing the above, we will reflect the key points of obtaining a social deduction for dental services:

- Expenses can be reimbursed only if the person had an income at the rate of 13% in the current year. Individual entrepreneurs in special regimes cannot use this benefit;

- The services rendered must be included in a special list (dental services, including expensive ones, are reflected in this list);

- A medical institution or individual entrepreneur must have a license and be located on the territory of the Russian Federation;

- Expenses can be reimbursed not only for yourself, but also for the next of kin (parents, children, spouses);

- The total tax refund period should not exceed 4 months (3 months for KNP and 1 month for a refund);

- You can only return personal income tax for treatment performed within the last three years. The balance of the deduction for the next year is not carried over;

- From 2016, it will be possible to receive a deduction through the employer in the tax period in which the expenses were made.