The Net present value, or NPV, indicator of an investment project allows you to determine what income an investor will receive in monetary terms as a result of his investments. In other words, the NPV of a project shows the amount of financial income as a result of investments in an investment project, taking into account associated costs, that is, net present value. What NPV is in practice and how to calculate net present value will become clear from the NPV formula below and its explanations.

Concept and content of NPV value

Before moving on to the topic of NPV, talking about what it is and how to calculate it, you need to understand the meaning of the phrase that makes up the abbreviation. For the phrase “Net present value” in the domestic economic and mathematical literature you can find several traditional translation options:

- In the first version, typical for mathematical textbooks, NPV is defined as net present value (NPV).

- The second option - net present value (NPV) - along with the first, is considered the most used.

- The third option – net present value – combines elements of the first and second transfers.

- The fourth version of the translation of the term NPV, where PV is “current value,” is the least common and is not widely used.

Regardless of the translation, the NPV value remains unchanged, and this term means that

NPV is the net present value of value. That is, cash flow discounting is precisely considered as the process of establishing its (flow) value by bringing the cost of total payments to a certain (current) point in time. Therefore, determining the net value (NPV) becomes, along with IRR, another way to estimate in advance.

At the level of the general algorithm, in order to determine the prospects of a business project according to this indicator, the following steps need to be taken:

- evaluate the movement - initial investments and expected revenues,

- set the cost of capital - calculate the rate,

- discount incoming and outgoing cash flows at an established rate,

- sum up all discounted flows, which will give the NPV value.

If the NPV calculation shows values greater than zero, then the investment is profitable. Moreover, the larger the NPV number, the greater, other things being equal, the expected profit value. Given that the lenders' return is usually fixed, anything the project brings in above it belongs to the shareholders - with a positive NPV, the shareholders will earn. The opposite situation with NPV less than zero promises losses for investors.

It is possible that the net present value will be zero. This means that the cash flow is sufficient to replace the invested capital without profit. If a project with an NPV of zero is approved, the size of the company will increase, but the share price will remain unchanged. But investing in such projects may be related to the social or environmental objectives of the initiators of the process, which makes investing in such projects possible.

NPV formula

Net present value is calculated using a calculation formula, which in a simplified form looks like PV - ICo, where PV represents the current cash flow indicators, and ICo is the size of the initial investment. In a more complex form, which shows the discounting mechanism, the formula looks like this:

NPV= - ICo + ∑ n t=1 CF t / (1 + R) t

Here:

Here:

- NPV– net present value.

- CF – Cash Flow is the cash flow (investment payments), and t next to the indicator is the time during which the cash flow occurs (for example, an annual interval).

- R – Rate– discount (rate: coefficient that discounts flows).

- n– the number of stages of project implementation, which determines the duration of its life cycle (for example, the number of years).

- ICo – Invested Capital– initial invested capital.

Thus, NPV is calculated as the difference between the total cash flows updated at a certain point in time by risk factors and the initial investment, that is, investor profit is considered as the added value of the project.

Since it is important for an investor not only to make a profitable investment, but also to competently manage capital over a long period of time, this formula can be further expanded to include not one-time, but additional periodic investments and an inflation rate (i)

NPV= ∑ n t=1 CF t / (1 + R) t - ∑ m j =1 IC j / (1 + i) j

Example of NPV calculation

An example calculation for three conditional projects allows you to both calculate NPV and determine which of the projects will be more attractive for investment.

According to the example conditions:

- initial investments - ICo - in each of the three projects are equal to 400 USD,

- profit rate – – is 13%,

- the profits that projects can bring (by year) are listed in the table for a 5-year period.

Let's calculate net present value to choose the most profitable project for investment. The discount factor 1/(1 + R) t for an interval of one year will be t = 1: 1/(1+0.13)1 = 0.885. If we recalculate the NPV of each scenario by year with the substitution of the defining values into the formula, it turns out that for the first project NPV = 0.39, for the second – 10.41, for the third – 7.18.

According to this formula, the second project has the highest net present value, therefore, if we are based only on the NPV parameter, then it will be the most attractive for investment in terms of profit.

However, the projects being compared may have different durations (life cycles). Therefore, there are often situations when, for example, when comparing three-year and five-year projects, the NPV will be higher for the five-year one, and the average value over the years will be higher for the three-year one. To avoid any contradictions, the average annual rate of return (IRR) must also be calculated in such situations.

In addition, the volume of initial investment and the expected profit are not always known, which creates difficulties in applying the calculations.

Difficulties in applying calculations

As a rule, in reality, the variables read (substituted into the formula) are rarely accurate. The main difficulty is determining two parameters: the assessment of all cash flows associated with the project and the discount rate.

Cash flows are:

- initial investment – initial outflow of funds,

- annual inflows and outflows of funds expected in subsequent periods.

Taken together, the amount of flow indicates the amount of cash that an enterprise or company has at its disposal at the current moment in time. It is also an indicator of the financial stability of the company. To calculate its values, you need to subtract Cash Outflows (CO), the outflow, from the value of Cash Inflows (CI) - cash inflow:

When forecasting potential revenues, it is necessary to determine the nature and degree of dependence between the influence of factors that form cash flows and the cash flow itself. The procedural complexity of a large complex project also lies in the amount of information that needs to be taken into account. So, in a project related to the release of a new product, it will be necessary to predict the volume of expected sales in units, while simultaneously determining the price of each unit sold. And in the long term, in order to take this into account, it may be necessary to base forecasts on the general state of the economy, the mobility of demand depending on the development potential of competitors, the effectiveness of advertising campaigns and a host of other factors.

When forecasting potential revenues, it is necessary to determine the nature and degree of dependence between the influence of factors that form cash flows and the cash flow itself. The procedural complexity of a large complex project also lies in the amount of information that needs to be taken into account. So, in a project related to the release of a new product, it will be necessary to predict the volume of expected sales in units, while simultaneously determining the price of each unit sold. And in the long term, in order to take this into account, it may be necessary to base forecasts on the general state of the economy, the mobility of demand depending on the development potential of competitors, the effectiveness of advertising campaigns and a host of other factors.

In terms of operational processes, it is necessary to predict expenses (payments), which, in turn, will require an assessment of prices for raw materials, rental rates, utilities, salaries, exchange rate changes in the foreign exchange market and other factors. Moreover, if a multi-year project is planned, then estimates should be made for the corresponding number of years in advance.

If we are talking about a venture project that does not yet have statistical data on production, sales and costs, then forecasting cash income is carried out on the basis of an expert approach. It is expected that experts should correlate a growing project with its industry counterparts and, together with the development potential, assess the possibilities of cash flows.

R – discount rate

The discount rate is a kind of alternative return that an investor could potentially earn. By determining the discount rate, the value of the company is assessed, which is one of the most common purposes for establishing this parameter.

The assessment is made based on a number of methods, each of which has its own advantages and initial data used in the calculation:

- CAPM model. The technique allows you to take into account the impact of market risks on the discount rate. The assessment is made on the basis of trading on the MICEX exchange, which determines the quotations of ordinary shares. In its advantages and choice of initial data, the method is similar to the Fama and French model.

- WACC model. The advantage of the model is the ability to take into account the degree of efficiency of both equity and borrowed capital. In addition to the quotations of ordinary shares, interest rates on borrowed capital are taken into account.

- Ross model. Makes it possible to take into account macro- and microfactors of the market, industry characteristics that determine the discount rate. Rosstat statistics on macroindicators are used as initial data.

- Methods based on return on equity, which are based on balance sheet data.

- Gordon model. Using it, an investor can calculate dividend yield, also based on quotes of ordinary shares, and also other models.

The change in the discount rate and the amount of net present value are related to each other by a nonlinear relationship, which can simply be reflected on a graph. Hence the rule for the investor follows: when choosing a project - an investment object - you need to compare not only the NPV values, but also the nature of their change depending on the rate values. The variability of scenarios allows an investor to choose a less risky project for investment.

Since 2012, at the instigation of UNIDO, the calculation of NPV has been included as an element in the calculation of the index of the rate of specific increase in value, which is considered the optimal approach when choosing the best investment decision. The assessment method was proposed by a group of economists headed by A.B. Kogan, in 2009. It allows you to effectively compare alternatives in situations where it is not possible to compare using a single criterion, and therefore the comparison is based on different parameters. Such situations arise when the analysis of investment attractiveness using traditional NPV and IRR methods does not lead to clear results or when the results of the methods contradict each other.

NPV is an indicator for assessing the economic efficiency of an investment project. It is calculated for both real and financial investments. See the example of how to calculate NPV and what conclusions about the effectiveness of the project can be drawn based on the calculation. And also download instructions for evaluating investment projects.

NPV is one of the main indicators used to evaluate the effectiveness of investment projects. Any error made in its calculation can lead to the launch of potentially ineffective investments. This article will help you correctly calculate and analyze the indicator.

What is NPV

NPV is the net value of cash flows reduced to the time of project calculation. The NPV calculation formula allows you to evaluate the project’s own economic efficiency; it can also be used to compare investment objects. In Russia, another term is often used - net present value - NPV, although the use of the word “income” can be misleading - in this formula we are talking about cash flows.

NPV formula and calculation rules

The NPV formula looks quite impressive:

where CFt is the total cash flow in period t.

and i is the discount rate (reduction rate).

When calculating NPV using the formula, it is necessary to include all investments in outgoing flows, regardless of the point in time, since in the general case investments can be made many times during the project, and not just in the initial period.

What does NPV show?

The positive value of the calculated NPV indicator clearly indicates that the project is effective taking into account alternative investments. Negative NPV means that the project is unprofitable and investment in it is unprofitable. If the NPV is zero, then the project will bring neither income nor loss.

How to calculate NPV in Excel

Example of NPV calculation

For an example of calculation, let's take a general case - this is a project in which investments are made not only in the zero year, but also during its implementation, in our case in the zero and first periods (Table 1). It is calculated for four years, the first year corresponds to the zero period. Let's take it equal to 10%.Table 1. Data for calculation, million rubles.

|

Year (period) |

||||

|

Investments |

||||

|

Discount rate |

||||

|

Discounted cash flow of the project |

||||

|

Cumulative discounted cash flow |

Let's calculate the net value of cash flows using the NPV formula given above:

NPV = (0-30-100) : (1+10%) 0 + (100-50-50) : (1+10) 1 +(160-80) : (1+10%) 2 + (220- 110) : (1+10%) 3 = -130: (1+10%) 0 + 0: (1+10) 1 +80: (1+10%) 2 + 110: (1+10%) 3 = 18.69 million rubles.

Conclusion: the project is effective, since in total, taking into account discounting, we have accumulated 18.69 million rubles in our accounts. .

Discount rate when calculating NIP

In our example, the discount rate was taken out of the blue, but in reality, its choice greatly influences the performance. And if we had taken not 10% interest, but 20%, then the project would have gone into negative territory (-10.82 million rubles) and would have become ineffective. When studying NPV, there is no way to avoid the issue of choosing a discount rate!

The discount rate, one of the names of which is the opportunity cost of investment, reflects the minimum return that an investor would like to receive at the same level of risk as the project being analyzed.

If an investor invests only his own funds, then the rate reflects his (the investor’s) assessment of the riskiness of the project. There are several options for estimating this value, the simplest and most understandable of which are the following:

- risk-free rate adjusted for specific risks. The risk-free rate can be the yield on bonds of the country where the project is implemented;

- the rate of return on bonds of companies in the same industry;

- required by the investor .

The logic for an investor when choosing a discount rate may be as follows:

- “I invest the available funds that I would otherwise leave on deposit at the bank, so I use the deposit rate as the opportunity cost of money.”

- “I invest temporarily free money, withdrawing it from the main business, but in the future I may need it again, and I will not be able to take it out of the project, therefore, I will use credit rates on the market as the cost of money.”

- “The average profitability of my business is N%, this will be the rate that I use as the discount rate, since I am not interested in receiving less than my main business brings.”

In most cases, the investor's rate of return is greater than the cost of borrowing. That is why, when financing a business, they often prefer to take out loans rather than attract an investor - he wants to get more for his hard-earned money than a specialized organization with a wide range of funding at low rates.

The discount rate at which NPV turns to zero is called the internal rate of return - IRR (internal rate of return). It shows the maximum cost of investment at which the project is effective.

Conclusion: the project is effective, since in total, taking into account discounting, we have accumulated 18.69 million rubles in our accounts.

Conclusion

NPV is the main indicator for analyzing the effectiveness of a project in comparison with investments in alternative assets. A positive value indicates that it is more profitable to implement the project than to invest in other assets with the same period and risk parameters. It must be understood that the indicator is based on cash flow forecasts, which in turn are subject to risks and are formed under conditions of uncertainty. Risks are partly taken into account by the discount rate.

Let's expand on the concept of net present value (NPV) of an investment project, give a definition and economic meaning, use a real example to look at calculating NPV in Excel, and also consider a modification of this indicator (MNPV).

Net present value(NPVNetPresentValue, net present value, net present value)– shows the effectiveness of an investment in an investment project: the amount of cash flow during the period of its implementation and reduced to the current value (discounting).

Net present value. Calculation formula

where: NPV – net present value of the investment project;

CF t (Cash Flow) – cash flow in time period t;

IC (Invest Capital) – investment capital represents the investor’s expenses in the initial time period;

r – discount rate (barrier rate).

Making investment decisions based on the NPV criterion

The NPV indicator is one of the most common criteria for evaluating investment projects. Let us consider in the table what decisions can be made at different NPV values.

Calculate and forecast future cash flow (CF) in Excel

Cash flow represents the amount of cash that a company/enterprise has at a given point in time. Cash flow reflects the financial strength of a company. To calculate cash flow it is necessary from the cash inflow (CI,Cash Inflows) means to take away the outflow (CO,Cash Outflows) , the calculation formula will look like this:

![]()

Determining the future cash flow of an investment project is very important, so let’s consider one of the forecasting methods using MS Excel. Statistical forecasting of cash flows is only possible if the investment project already exists and is operating. That is, funds are needed to increase its capacity or scale it. I would like to note that if the project is a venture project and does not have statistical data on production volumes, sales, costs, then an expert approach is used to assess future cash income. Experts compare this project with analogues in this area (industry) and assess the potential for possible development and possible cash flows.

When forecasting the volume of future receipts, it is necessary to determine the nature of the relationship between the influence of various factors (forming cash receipts) and the cash flow itself. Let's look at a simple example of predicting future cash flows from a project depending on advertising costs. If there is a direct relationship between these indicators, then you can predict what cash receipts will be depending on costs using linear regression in Excel and the “TREND” function. To do this, we write the following formula for advertising costs of 50 rubles.

Cash Flow (CF). B12=TREND(B4:B11,C4:C11,C12)

The size of the future cash flow will be 4831 rubles. with advertising costs of 50 rubles. In reality, determining the size of future revenues is influenced by a much larger number of factors, which should be selected according to the degree of influence and their relationship with each other using correlation analysis.

Determining the discount rate (r) for an investment project

Calculating the discount rate is an important task in calculating the current value of an investment project. The discount rate represents the alternative return that an investor could have received. One of the most common purposes for determining a discount rate is to estimate the value of a company.

To estimate the discount rate, methods such as the CAPM model, WACC, Gordon model, Olson model, E/P market multiples model, return on equity, Fama and French model, Ross model (ART), expert assessment, etc. are used. There are many methods and their modifications for estimating the discount rate. Let us consider in the table the advantages and initial data that are used for the calculation.

| Methods | Advantages | Initial data for calculation |

| CAPM model | Taking into account the impact of market risk on the discount rate | |

| WACC model | The ability to take into account the efficiency of using both equity and borrowed capital | Quotations of ordinary shares (MICEX exchange), interest rates on borrowed capital |

| Gordon model | Accounting for dividend yield | Quotations of ordinary shares, dividend payments (MICEX exchange) |

| Ross model | Taking into account industry, macro and micro factors that determine the discount rate | Statistics on macro indicators (Rosstat) |

| Fama and French model | Taking into account the impact on the discount rate of market risks, the size of the company and its industry specifics | Quotations of ordinary shares (MICEX exchange) |

| Based on market multiples | Accounting for all market risks | Quotations of ordinary shares (MICEX exchange) |

| Based on return on equity | Accounting for the efficiency of using equity capital | Balance sheet |

| Based on expert assessment | The ability to evaluate venture projects and various factors that are difficult to formalize | Expert assessments, rating and point scales |

A change in the discount rate has a non-linear effect on the change in net present value; this relationship is shown in the figure below. Therefore, when choosing an investment project, it is necessary not only to compare NPV values, but also the nature of the change in NPV at different rates. Analysis of various scenarios allows you to choose a less risky project.

Calculate Net Present Value (NPV) Using Excel

Let's calculate net present value using Excel. The figure below shows a table of changes in future cash flows and their discounting. So, we need to determine the discount rate for a venture investment project. Since it has no issues of ordinary shares, no dividend payments, and no estimates of return on equity and debt capital, we will use the method of expert assessments. The evaluation formula will be as follows:

Discount rate=Risk-free rate + Risk adjustment;

Let's take a risk-free rate equal to interest on risk-free securities (GKOs, OFZs, these interest rates can be viewed on the website of the Central Bank of the Russian Federation, cbr.ru) equal to 5%. And adjustments for industry risk, the risk of the impact of seasonality on sales and personnel risk. The table below shows estimates of adjustments taking into account these identified types of risk. These risks have been identified by experts, so when choosing an expert you need to pay close attention.

| Types of risk | Risk adjustment |

| Risk of seasonality affecting sales | 5% |

| Industry risk | 7% |

| Personnel risk | 3% |

| 15% | |

| Risk-free interest rate | 5% |

| Total: | 20% |

As a result, adding up all the adjustments for the risk affecting the investment project, the discount rate will be = 5 + 15 = 20%. After calculating the discount rate, it is necessary to calculate the cash flows and discount them.

Two options for calculating net present value NPV

The first option for calculating net present value consists of the following steps:

- Column “B” reflects the initial investment costs = 100,000 rubles;

- Column “C” reflects all future planned cash receipts for the project;

- Column "D" records all future cash expenses;

- Cash flow CF (column “E”). E7= C7-D7;

- Calculation of discounted cash flow. F7=E7/(1+$C$3)^A7

- Calculate the present value (NPV) minus the initial investment cost (IC). F16 =SUM(F7:F15)-B6

The second option for calculating net present value is to use Excel's built-in NPV (net present value) financial function. Calculation of the net present value of a project minus initial investment costs. F17=NPV($C$3;E7;E8;E9;E10;E11;E12;E13;E14;E15)-B6

The figure below shows the resulting net present value calculations. As we can see, the final result of the calculation is the same.

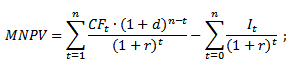

Modification of net present value MNPV (Modified Net Present Value)

In addition to the classic net present value formula, financiers/investors sometimes use its modification in practice:

MNPV – modification of net present value;

CF t – cash flow in time period t;

I t – cash outflow in time period t;

r – discount rate (barrier rate);

d – level of reinvestment, interest rate showing possible income from reinvestment of capital;

n – number of analysis periods.

As we see, the main difference from the simple formula is the possibility of taking into account the profitability from reinvestment of capital. Evaluation of an investment project using this criterion has the following form:

Advantages and disadvantages of the net present value valuation method

Let's compare the advantages of the NPV and MNPV indicators. The advantages of using these indicators include:

- Clear boundaries for choosing and assessing the investment attractiveness of the project;

- Possibility of taking into account additional project risks in the formula (discount rate);

- Using a discount rate to reflect changes in the value of money over time.

The disadvantages of net present value include the following:

- Difficulty in assessing complex investment projects that involve many risks;

- Difficulty in accurately forecasting future cash flows;

- No influence of intangible factors on future profitability (intangible assets).

Summary

Despite a number of shortcomings, the net present value indicator is key in assessing the investment attractiveness of a project, comparing it with analogues and competitors. In addition to estimating NPV, for a clearer picture, it is necessary to calculate investment ratios such as IRR and DPI.

When a person receives an offer to invest in a project, he cannot be sure of its profitability. Net present value will help determine the amount of income from an investment.

Net present value: concept, basic information

Net present value (NPV) is an indicator of the effectiveness of investments in any investment project.

To calculate the NPV, use the formula:

- CF represents cash flow.

It should be calculated as the amount of investment for each period of time (depending on the duration of the investment period itself); - IC stands for Investor's Capital.

This value is always indicated with a “-“ sign.As a rule, the investor does not deposit the entire amount at once, but pays the money as needed.

In this regard, these contributions must be discounted, taking into account the time interval; - r is the discount rate.

This value allows you to calculate the possible total amount of income at this moment.

Once you know the size of the NPV, you can assess how profitable it will be to invest in a particular project.

So, if the NPV indicator is:

- negative, that is, ˂0, then this investment is unprofitable.

With a negative indicator, the investor will not only be unable to replenish his budget with additional funds, but will also lose his money; - is 0, then the investment will bring neither income nor loss.

In other words, by investing his own funds in a program with a “zero” NPV indicator, the investor will not receive even the smallest income, but he will not incur losses either; - positive, that is, ˃0, then the business idea will bring profit to the investor.

But if you are offered to invest in several projects, then you need to calculate the NPV of each of them and finance the one that is the most profitable.

It is worth noting that this indicator shows profit or loss for the entire investment period.

The video will help you calculate net present value.

What is net present value used for?

The NPV indicator is the main factor that an investor pays attention to when planning his investments in a particular program. Only by calculating discounted income is a decision made on the advisability of investment.

When choosing a project to invest their own funds, the investor must analyze:

- investment period;

- amount of income;

- type of business.

And the NPV number allows you to find out the real effectiveness of your investment, omitting all the above factors. Thanks to this indicator, it is clearly visible which of the proposed projects can bring more profit.

In addition, the amount of money you are now planning to invest may have a lower true value before the end of the investment period than it currently has. There is also always a risk that, despite detailed calculations, your investment may not bring you the expected amount of profit.

Calculation using the formula and explanation of the value

The amount of NPV should be calculated as the sum of all expenses and income. This calculation assumes that the discount rate will be a satisfactory rate of return per 1 ruble for the investor.

This norm must be objective, because it takes into account:

- inflation rate;

- interest on bank deposits;

- average income from securities;

- investor's personal forecast;

- the cost of all capital investments (this is necessary when the project will be invested by more than one investor).

The NPV indicator itself is according to the following scheme:

- first, the investor must determine the amount he is willing to invest in the project;

- at the next stage it is necessary to calculate the amount of planned cash flows from the project;

- Next, the investor must calculate the total amount of planned cash receipts, taking into account the time of the first expected income;

- and, finally, the amount of all expenses must be compared with the amount of income.

How to calculate correctly using an example

To understand how the NPV is calculated, let's look at a specific example. In our example, the discount rate is 12%.

For convenience, we present the indicators of cash injections by year in the table.

Now let’s substitute all these values into the formula we know:

As you can see, by investing money in this project, the investor will not only not be able to make a profit, but will also incur losses.

Every investment must make economic sense. Simply put, all cash flows are brought to the present moment, and then their amount is calculated.

If the result is negative, then it turns out that the investor will have to invest more than he receives. In this case, the investor refuses to finance such a project.

To ensure that when calculating the NPV indicator, the NPV is justified and reflects real profitability, it is very important to use the most accurate source data. To do this, it is recommended to use a production, financial or marketing plan, which contains information that is as close as possible to real conditions.

As mentioned above, the return on investment is highly dependent on inflation. But how can you predict the inflation rate at the time of completion of the investment project?

Adjusting the discount to the expected percentage of inflation will help with this.

To find out the rate, use the following formula:

- R denotes the discount rate;

- r is the discount;

- j is the inflation rate.

It is clear from the formula that profitability during inflation may be lower so that the project continues to maintain its prospects and make a profit.

Pros and cons of net present value

Although NPV is the only way to assess the profitability of a project, this method also has its drawbacks.

These include:

- Cash flow figures may not reflect actual results.

A person sees only expected values.And no one knows exactly how the economic situation will change in a month or a year.

- It is not always possible to calculate an accurate discount rate.

This is especially true for multidisciplinary projects.

Still, NPV has many advantages.

These can include:

- the ability to find out the value of cash investments relative to a certain period;

- the ability to calculate all possible risks throughout the entire period of implementation of the investment project.

From all of the above, we can conclude that the NPV indicator is a convenient way to calculate which of the proposed investment projects will be the most profitable.

In contact with

To assess the effectiveness of the project, the company's economists simulate the circulation of invested capital. In order to build models, cash flow and cash flow discounting methodologies are used. The basic parameter of the financial model of a project business plan is NPV, which we will consider in this article. This criterion came into economic analysis in the early nineties and to this day occupies the first position in the comprehensive and comparative assessment of projects.

Basics of project effectiveness assessment

Before we move directly to understanding NPV (net present value), I would like to briefly recall the main points of the evaluation methodology. Its key aspects make it possible to most competently calculate a group of project performance indicators, including NPV. Among the project participants, the main figure interested in evaluation activities is the investor. His economic interest is based on the awareness of the acceptable rate of return that he intends to extract from the actions of placing funds. The investor acts purposefully, refusing to consume available resources, and counts on:

- return of investment;

- compensation for your refusal in future periods;

- better conditions in comparison with possible investment alternatives.

By the rate of return beneficial to the investor, we will understand the minimum acceptable ratio of capital growth in the form of the company’s net profit and the amount of investment in its development. This ratio during the project period should, firstly, compensate for the depreciation of funds due to inflation, possible losses due to the occurrence of risk events, and secondly, provide a premium for abandoning current consumption. The size of this premium corresponds to the entrepreneurial interests of the investor.

The measure of entrepreneurial interest is profit. The best prototype of the profit generation mechanism for the purpose of evaluating an investment project is the flow methodology for reflecting cash flows (CF) from the perspective of income and expense parts. This methodology is called cash flow (CF or cash flow) in Western management practice. In it, income is replaced by the concepts of “receipts”, “inflows”, and expenses - “disposals”, “outflows”. The fundamental concepts of cash flow in relation to an investment project are: cash flow, settlement period and calculation step (interval).

Cash flow for investment purposes shows us the receipts of assets and their disposals arising in connection with project implementation during the entire duration of the billing period. The period of time during which it is necessary to track the cash flows generated by the project and its results in order to evaluate the effectiveness of the investment is called the calculation period. It represents a duration that may extend beyond the time frame of the investment project, including the transition and operational phases, until the end of the equipment life cycle. Planning intervals (steps) are usually calculated in years; in some cases, for small projects, a monthly interval breakdown can be used.

Methods for calculating net income

Of great importance for calculating NPV and other project indicators is how income and expenses are generated in the form of inflows and outflows of business assets. The cash flow methodology can be applied in a generalized form or localized by groups of cash flows (in operational, investment and financial aspects). It is the second form of presentation that makes it possible to conveniently calculate net income as the simplest parameter for assessing efficiency. Next, we present to your attention a model of the relationship between the classical grouping of DS flows and grouping according to subject-target characteristics.

Scheme of two variants of groupings of DS flows with interconnections

The nature of the content of the economic effect of investments is expressed in the comparison of the total inflows and outflows of funds at each calculated step of the project task. Net income (CF or BH) is calculated for the corresponding interval value i. Below are the formulas for calculating this indicator. The dynamics of black holes are almost always repeated from project to project. For the first one or two steps, the ND value is negative, because the results of operating activities are not able to cover the size of the investments made. Then the sign changes, and in subsequent periods net income increases.

Formula for calculating net income for period i

The cost of DS changes over time. This is due not only to inflation, but also to the fact that money itself can generate a certain income. Therefore, the blackout should be brought to the time of the start of the project through the discounting procedure, which uses the net present value method. Thanks to it, ND receives the status of a new indicator called “net present value” or “net present value”. We are no longer interested in step-by-step, but in cumulative discounted cash flow. Its formula is presented below.

Formula for total discounted cash flow

The parameters “discount rate”, “discounted cash flow”, “discount factor” will be discussed in separate material, revealing their financial and economic nature. I will only note that guidelines for the value of r in a project can be the levels of the WACC indicator, the Central Bank refinancing rates, or the rate of return for an investor who is able to secure more profitable alternative investments. The total discounted cash flow can be interpreted and the net present value (NPV) can be calculated from it.

NPV formula

NPV shows us how much money an investor will be able to receive after the size of investments and regular outflows reduced to the initial moment are covered by the same inflows. The “net present value” indicator serves as a successful replica of the Western NPV indicator, which became widespread in Russia during the “boom” of business planning. In our country, this indicator is also called “net present value”. Both English and Russian interpretations of the NPV indicator are equally widespread. The NPV formula is shown below.

NPV formula for the purpose of assessing the effectiveness of a project activity

The net present value presented in the formula is the subject of much debate among practitioners. I do not pretend to have the truth, but I believe that domestic methodologists will have to bring some clarity to a number of issues and, perhaps, even correct textbooks. I will express only a couple of comments regarding the main nuances.

- To calculate the “net present value” indicator, one should rely on the classical understanding of net cash flow (NCF) as a combination of operating, investment and financial flows. But investments should be separated from NCF, since common sense discount factors may be different for the two parts of this formula.

- When calculating NPV (NPV), dividends associated with the project must be excluded from the NCF, since they serve as a form of withdrawal of the investor’s final income and should not affect the NPV value of the project.

Net present value, based on these comments, can have several interpretations of the formula, one of which is the option when the discount rate in relation to the size of the investment is based on the WACC or the percentage of inflation. At the same time, the base part of the NCF, adjusted to the initial period at the rate of return, significantly reduces the net present value. The investor’s increased demands on the level of rate r has its consequences, and the net present value decreases or even reaches negative values.

Net present value is not an exclusive indicator of performance and should not be considered in isolation from a group of other criteria. However, NPV represents the main evaluation parameter due to its ability to express the economic impact of a project. Even if the indicator turns out to be slightly above zero, the project can already be considered effective. The formula for calculating NPV in the traditional form of the Western school of management is presented below.

Formula for the net present value of a project

Example of NPV calculation

As we have established, the discount factor carries the investor’s expectations for income from the project. And if during the billing period all project costs are covered by income taking into account discounting, the event is able to satisfy these expectations. The sooner such a moment comes, the better. The higher the net present value, the more effective the project. NPV shows how much additional income an investor can expect. Let's look at a specific example of calculating NPV. Its main initial conditions are:

- the value of the calculation period is 6 years;

- selected planning step – 1 year;

- the moment of starting investment corresponds to the beginning of step “0”;

- the need to obtain borrowed funds is ignored; for simplicity, we assume that investments were made at the expense of the company’s own capital, i.e. CF from financing activities is not taken into account;

- Two options for the discount rate are considered: option A, where r=0.1; option B, where r=0.2.

All initial data on investments and operating CF by project year are given in the table presented.

Example data for calculating the NPV of a project

As a result of filling out the bottom three rows of the table, we are able to calculate the indicators.

- The net income of the project amounted to 3,000 thousand rubles (-300+200+600+1100+1900+2500-3000).

- Net present value for r=0.1, amounting to 687 thousand rubles (-272+165+451+751+1180+1412-3000).

- For the discount rate, r=0.2 amounts to -634 thousand rubles (-250+139+347+530+763+837-3000).

If we compare the three obtained values, the conclusion suggests itself that with a rate of return of 10%, the project can be considered effective, while the investor’s demands for a rate of 20% exclude this event from the zone of his interests. This happens quite often. In recent years, in our economy, the value of the real rate of return has been steadily declining, so relatively few strategic investors come, mainly speculative ones.

In this article, we examined the most popular indicator of assessment, analysis of the economic efficiency of investments and project practice - NPV. When calculating the indicator, the net present value method is used, which allows you to adjust the cash flows generated in the project to changes in the time value of money. The advantage of this criterion is its ability to find an investment effect that is adequate to economic realities, and the disadvantage is its closeness to the investor’s subjective view of the level of expected profitability.