Return on equity reflects the ratio of net profit from sales to the average amount of equity.

The data for calculation is taken from the balance sheet. The profitability ratio is designated "ROE".

Economic meaning of the financial indicator “ROE”

The profitability ratio shows how effectively the invested money was used in the reporting period. It is clear that this indicator is extremely important for investors and business owners.

There are several profitability ratios. We will be interested in return on equity. That is, those assets that belong to the company as a property.

How to evaluate the calculation result:

- The higher the ratio, the more efficiently the invested funds were used. Investments are more profitable.

- Too high an indicator – the financial stability of the organization “suffers”.

- The coefficient is below zero - the feasibility of investing in this enterprise is questionable.

The return on equity ratio is compared with other options for investing free money in assets and securities of other companies. Or with bank interest on deposits, as a last resort.

The value of return on equity.

Formula for calculating ROE in Excel

The return on equity is calculated as the quotient of net profit to the average amount of equity investments. Data is taken for a certain time interval: month, quarter, year.

Formula for calculating the return on equity ratio:

ROE = (Net profit / Average equity) * 100%.

The figures for calculations must be taken from the income statement (total indicator) and the liabilities side of the balance sheet (total indicator).

Average equity capital - calculation formula:

SK = (SK of the beginning of the period + SK of the end of the period) / 2.

Return on equity – balance sheet formula:

ROE = (line 2110 + line 2320 + line 2310 + line 2340) / ((line 1300 ng + line 1300 kg + line 1530 ng + line 1530 kg) / 2) * 100%.

The numerator contains data from the financial performance statement (Form 2). The denominator is from the final balance sheet (Form 1).

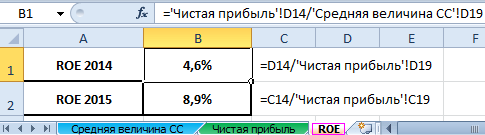

To calculate profitability using Excel, we enter data for the financial statements of company “X”:

And the financial results statement (“in the old way”: profit and loss):

The tables highlight the values that will be needed to calculate the return on equity ratio.

- Profitability ratio for 2015: = (6695 / 75000) * 100% = 8.9%.

- Profitability ratio for 2014: = (2990 / 65000) * 100% = 4.6%.

We automate the calculation using Excel formulas. In general, you can make a separate table with important economic indicators. Enter formulas with links to values in the corresponding reports - and quickly obtain data for statistical analysis, comparison and management decisions.

Excel formulas for calculating return on equity:

Conclusions:

- There is an increase in the return on equity from 4.6 percent to 8.9 percent.

- It is not profitable to invest available funds in shares of company X. The same bank deposit rate in 2015 was 9.5%.

- It is advisable to consider other offers from companies or put money on deposit at interest (as a last resort).

The investment attractiveness of a project is not assessed only by the return on investment. When making a decision, the investor looks at return on assets, sales and other criteria for the efficiency of the enterprise.

Material from the site

What is Return on Equity

Return on equity (ROE), also used the term "return on equity") - a financial ratio that shows the return on investment of shareholders in terms of accounting profit. This accounting measurement method is similar to return on investment (ROI).

This relative performance indicator is expressed in the formula:

The net profit received for the period is divided by the organization's equity capital.

The amount of net profit is taken for the financial year, excluding dividends paid on ordinary shares, but taking into account dividends paid on preferred shares (if any). Share capital is taken without taking into account preference shares.

The benefits of ROE ratio

The financial return indicator ROE is important for investors or business owners, since it can be used to understand how effectively the capital invested in the business was used, how effectively the company uses its assets to generate profit. This indicator characterizes the efficiency of using not the entire capital (or assets) of the organization, but only that part of it that belongs to the owners of the enterprise.

However, Return on Equity is an unreliable measure for determining the value of a company, as it is believed that this indicator overestimates economic value. There are at least five factors:

1. Duration of the project. The longer it takes, the more inflated the indicators are.

2. Capitalization policy. The smaller the share of capitalized total investments, the greater the overstatement.

3. Depreciation rate. Uneven depreciation results in higher ROE.

4. The lag between investment costs and the return from them through cash inflows. The greater the time gap, the higher the degree of overestimation.

5. Growth rate of new investments. Fast-growing companies have lower Return on Equity.

The coefficient is equal to the ratio of net profit from sales to the average annual cost of equity capital. Data for calculation - balance sheet.

It is calculated in the FinEkAnalysis program in the Profitability Analysis block as Return on Equity.

Return on equity - what it shows

Shows the amount of profit that the company will receive per unit of equity capital value.

Return on Equity - Formula

General formula for calculating the coefficient:

Calculation formula based on the old balance sheet data:

Return on equity - value

(K dsk) is essentially the main indicator for strategic investors (in the Russian sense - investors of funds for a period of more than a year). The indicator determines the efficiency of using capital invested by the owners of the enterprise. Owners receive return on investment in the form of contributions to the authorized capital. They donate those funds that form the organization’s own capital and in return receive rights to a corresponding share of profits.

From the perspective of owners, profitability is most reliably reflected in the form of return on equity. The indicator is important for the company’s shareholders, as it characterizes the profit that the owner will receive from a ruble investment in the enterprise.

There are limitations to the use of this coefficient. Income does not come from assets, but from sales. Based on K DSC, it is impossible to assess the efficiency of a company's business. In addition, most companies use a significant proportion of debt capital. As an accounting metric, Return on Equity provides insight into the earnings a company earns for shareholders.

The return on equity is compared with possible alternative investments in shares of other enterprises, bonds, bank deposits, etc.

The minimum (normative) level of profitability of an entrepreneurial business is the level of bank deposit interest. The minimum standard value of the Return on Equity indicator (K dsk) is determined by the following formula:

K rna = Cd*(1-Snp)

- K rnk – standard value of return on equity capital, relative units;

- SD – average rate on bank deposits for the reporting period;

- STP – income tax rate.

If the Kdsk indicator for the analysis period turned out to be lower than the minimum Krnk or even negative, then it is not profitable for the owners to invest in the company. An investor should consider investing in other companies.

To make the final decision on exiting the company’s capital, it is better to analyze K DSC for recent years and compare it with the minimum level of profitability for this period.

Return on equity - diagram

Was the page helpful?

Synonyms

More found about return on equity

- Assessing the premium for a company's specific risks when determining the required return on equity

TCOE total cost of equity - return on the asset being valued or rate of cost of equity capital Rf - return on the risk-free asset RPm - premium for market risk RPs - - Subject-oriented approach to assessing the required return on equity

The required return on equity capital is today the most important parameter for making investment decisions, both in - Valuation of shares and the value of commercial organizations based on a new financial reporting model

E required return on equity capital SK 0stP extended value of residual profit in the post-forecast period Amount of residual profit - Factors of company-specific risks when assessing the premium for these risks in emerging capital markets

In the future, this will lead to a more adequate assessment of the required return on the company's equity capital, unsystematic risk, taking into account all its risks. Conclusions Operational and financial -

Return on equity capital Return on equity capital is a coefficient equal to the ratio of net profit from sales to the average annual cost - Analysis of capital valuation models

Almost 80% of companies around the world use this model to estimate the expected return on equity capital. Although CAPM is based on fairly strict assumptions that are unlikely - Assessment of the value of an enterprise's equity capital taking into account the financial risk of an investment project

If the basic and alternative projects have approximately the same level of financial risk, then the cost of equity for the basic project can be taken equal to the return on equity when implementing the alternative project where FRLb is the level of financial risk of the main project - How much is the company's equity worth?

SDR - market return on equity capital % per year β - beta coefficient characterizing the risk of investment in a company - Methods for assessing the value of a company in M&A transactions using the example of the takeover of JSC CONCERN KALINA

CAPM re rf β ERP 1 where re is the expected return on equity rf is the risk-free rate of return β is a measure of systematic risk ERP premium - Capital asset valuation model as a tool for estimating discount rates

Solving equation 3 for ke, we obtain the return on equity from which it will then be necessary to subtract the risk-free rate. So, if we take the level - Income Statement Analysis - Part 2

Profit after interest 200 130 80 Return on equity 10% 13% 8% Return on equity will be calculated as the ratio of profit after interest - Return on equity

Synonyms return on equity capital return on equity capital is calculated in the FinEkAnalysis program in the Profitability Analysis block as Return on equity capital -

- Two contours of interests in the company’s financial health policy

Required return on equity capital Amount of equity capital employed The company is characterized as operating effectively within - Calculation of key financial indicators of business performance

WACC To find the cost of equity capital, we calculate the rate of return on equity capital using the CAPM 4 capital asset valuation model. Moreover, the data - Assessing the efficiency of using an enterprise's own and borrowed capital

According to the methodology for analyzing the return on equity using the effect of financial leverage, profitability can be presented in the following form - Risk premium cancels depreciation and multiplies prices

In Russia and abroad, methods for assessing the value of property of the equity capital of a business based on the income method imply the use of the capitalization rate by the cumulative construction method with -

Dj value of the jth source of borrowed investment capital r 1, 2, 3, n number of sources of equity investment capital j 1, 2, 3, m - number of sources of borrowed investment capital rd - minimum rate of return on borrowed investment capital re - minimum rate of return on equity investment capital The system of equations must be solved for D E or rd re -

Alpha will be in a difficult financial situation for this reason, also zero. The return on equity, taking into account the influence of financial leverage, will be 20% 20% 20% - 12% X - Methods for determining the discount rate when assessing the effectiveness of investment projects

The rate of return on equity can be calculated using the long term asset pricing model WACC is used in

The return on equity indicator ROE (Return On Equity) is one of the most important financial indicators for investors. Unlike the return on assets (ROA) indicator, ROE characterizes the efficiency of using not all of the company's capital, but only that part of it that belongs to its shareholders. Expressed as a percentage and calculated as:

- ROE = Net Profit / Equity Value x 100

- ROE = Net Income / Shareholder’s Equity x 100

The amount of net profit is taken for the financial year, excluding dividends paid on ordinary shares (taken into account when calculating the ROCE ratio), but taking into account dividends paid on preferred shares (if any). Share capital is taken without taking into account preference shares.

ROE is the rate at which a company's shareholders' funds work. So, if ROE = 20%, this means that for every dollar invested by shareholders, the company generated $0.20 in net income.

Comparing return on equity with return on assets (ROA) provides insight into financial leverage - debt financing

For ordinary shares, the return on common equity (ROCE) indicator is used. Expressed as a percentage and calculated as:

- ROCE = Net income – Preferred dividends / Cost of equity – Preferred shares x 100

- ROCE = Net Income – Preferred Dividends / Shareholder’s Equity – Preferred Stocks x 100

ROE should be compared to the ROE of similar companies, as well as to alternative investment options available in the market. If the company's ROE is consistently below market rates of return, then it is more advisable to liquidate the business and invest money in market assets.

As ROE increases, the P/B multiplier should also increase. Low ROE and high P/B may indicate that the stock is overvalued. High ROE and low P/B mean that the market underestimates the company's potential.

It is also important to consider that the company can improve its ROE ratio, buying back its own shares from the market, thereby reducing their number in circulation and increasing the return on equity. As a result, this may give the investor an erroneous impression of the issuer's business performance.

As for the standard value of ROE, in the long term the return on capital should not be lower than low-risk investments in financial instruments. Because if the return on capital of a business is lower than the rates on deposits in large banks or on bonds, then the business ceases to be profitable for its owners.

- For example, if it is expected that in the next 3 years deposit rates will be in the range of 8-10%, then any business that will bring 10-12% on capital is unpromising, since it must be taken into account that the risks of doing business are much higher, than investments in government bonds or deposits.

Thus, the prospects of a business are assessed taking into account rates on low-risk investments (bonds or deposits in large banks) and risk premiums (corporate, market, economic, political, etc.).

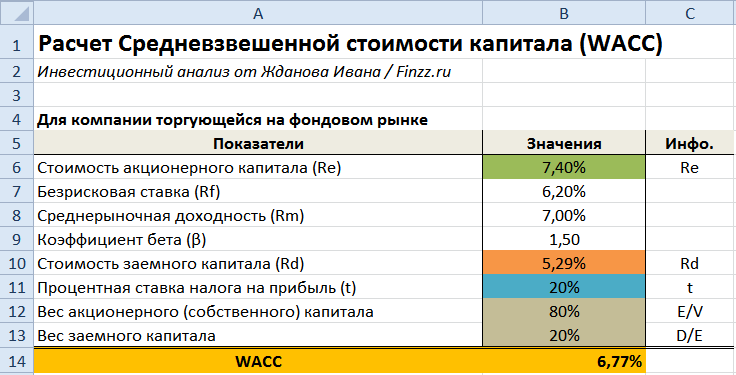

Weighted average cost of capital (eng. WACC, Weighted Average Cost of Capital, analogue: weighted average cost of capital) used to assess the return on capital of a company, the rate of profitability of an investment project and business. In this article we will look at how the weighted average cost of capital WACC is calculated in Excel using the capital asset pricing model (CAMP) and based on financial statements and balance sheets.

Formula for calculating the weighted average cost of capital

The essence of WACC is to estimate the cost (return) of a company's equity and debt capital. Own capital includes: authorized capital, reserve capital, additional capital and retained earnings. Authorized capital is the capital contributed by the founders. Reserve capital is money intended to cover losses and losses. Additional capital is money received as a result of the revaluation of property. Retained earnings are cash received after deducting all payments and taxes.

The formula for calculating the weighted average cost of capital WACC is as follows:

where: r e - return on equity capital of the organization;

r d - profitability of the organization's borrowed capital;

E/V, D/V – the share of equity and debt capital in the company’s capital structure. The sum of equity and debt capital forms the company's capital (V=E+D);

t – interest rate of income tax.

Areas of application of the weighted average cost of capital

WACC model is used in investment analysis as a discount rate in calculations of investment project performance indicators: NPV, DPP, IP. (⊕ )

In strategic management to assess the dynamics of changes in the value of an organization. To do this, WACC is compared to return on assets (ROA). If WACC>ROA, then economic value added (EVA) decreases and the company “loses” value. If WACC In assessing mergers and acquisitions M&A transactions. To do this, the WACC of the companies after the merger is compared with the sum of the WACCs of all companies before the merger. In business valuation, as a discount rate in assessing key indicators of a business plan. Let's consider the main problems of using the approach to estimating the weighted average cost of capital: The most difficult part of calculating the WACC indicator is calculating the return on equity (R e). There are many different approaches to assessment. The table below discusses the key models for assessing the performance of equity capital and the areas of their application ↓ Fama and French model Carhart model The cost of an organization's shareholder (equity) capital is calculated using the CAPM model using the formula: r is the expected return on the company's equity; r f – return on a risk-free asset; r m – return of the market index; β — beta coefficient (sensitivity of changes in stock returns to changes in market index returns); σ im is the standard deviation of the change in the stock’s return from the change in the return of the market index; σ 2 m – dispersion of market index returns. The return on the risk-free asset (Rf) can be taken as the yield on government OFZ bonds. Bond yield data can be viewed on the website rusbonds.ru. For the calculation we will use a coupon yield of 6.2%. The figure below shows the OFZ-PD bond card ⇓ Average market return (Rm) is the average return of the RTS or MICEX market index (on the Moscow Exchange website →). We took a yield of 7%. The beta coefficient shows the sensitivity and direction of changes in stock returns to market returns. This indicator is calculated based on the returns of the index and the stock. For more information about calculating the beta coefficient, read the article: →. In our example, the beta coefficient is 1.5, which means the stock is highly volatile relative to the market. The formula for calculating the value of equity (shareholder) capital is as follows: Cost of equity = B7+B9*(B8-B7) Cost of borrowed capital (Rd) - represents the fee for using borrowed funds. We can obtain this value based on the company’s balance sheet; an example of calculating these values is discussed below. The interest rate for income tax is 20%. The income tax rate may vary depending on the type of activity of the company. Different income tax rates The weight of equity and debt capital in the example was taken as 80 and 20%, respectively. The formula for calculating WACC is as follows: WACC = B6*B12+(1-B11)*B13*B10 In one of the stages of calculating the weighted average price of capital, it is necessary to calculate the projected return on equity (R e), which is usually calculated using the CAPM model. For the correct application of this model, it is necessary to have ordinary shares traded on the market. Since CJSC companies do not have public issues of shares, it is impossible to assess the return on capital using a market method. Therefore, return on equity can be assessed on the basis of financial statements - the ROE (return on equity) ratio. This indicator reflects the rate of return created by the company's equity capital. As a result, R e = ROE The WACC calculation formula will be modified. Let's look at an example of calculating WACC on an organization's balance sheet. This approach is used when a company does not issue ordinary shares on the stock market or they are low-volatile, which does not allow the return (efficiency) of the company’s capital to be assessed on the basis of a market approach. We will conduct the assessment based on the balance sheet of KAMAZ OJSC. Despite the fact that this company has ordinary shares, their market volatility is too weak to adequately assess the return on equity using the CAPM model. The organization's balance sheet can be downloaded from the official website or →. The first parameter of the formula is the cost of equity capital, which will be calculated as the organization’s return on equity. The calculation formula is as follows: Net profit is reflected in line 2400 in the income statement, the amount of equity capital in line 1300 of the balance sheet. Entering data into Excel. Cost of equity = B6/B7 At the next stage, it is necessary to calculate the cost of borrowed capital, which is a fee for the use of borrowed funds, in other words, the percentage that the organization pays for borrowed funds. Interest paid at the end of the reporting year is presented in line 2330 of the balance sheet, the amount of borrowed capital is the sum of long-term and short-term liabilities (line 1400 + lines 1500) in the income statement. The formula for calculating the cost of borrowed capital is as follows: Cost of borrowed capital =B9/B10 At the next stage, we enter the values of the tax percentage rate. The income tax rate is 20%. To calculate the shares of equity and borrowed capital, it is necessary to apply existing data and formulas: Equity weight = B7/(B7+B10) Debt capital weight = B10/(B7+B10) WACC = B5*B12+(1-B11)*B13*B8 Let's consider one of the options for modifying the formula for calculating the weighted average cost of capital. If an organization has preferred and ordinary shares on the stock market, then the formula for calculating WACC is modified: E/V – the share of ordinary shares owned by the organization; P/V – the share of preferred shares owned by the company; D/V – share of borrowed capital (Amount E+P+D=V); Re – return on ordinary shares; Rp – return on preferred shares; Rd – cost of borrowed capital; t – income tax. Summary The weighted average cost (price) of capital WACC model is relevant to use when calculating from financial statements, since in this case the return on equity is calculated on the balance sheet. If CAPM methods, Gordon's model, etc. are used to calculate return on equity, then the WACC value will be distorted and will not have practical application. The method is usually used to evaluate existing businesses, projects and companies and is less applicable to evaluate startups.Difficulties in applying the WACC method in practice

Methods for calculating return on equity

Methods and models

Application areas

Sharpe model (CAPM) and its modifications:

Used to assess return on equity for companies that issue ordinary shares on the stock market

(constant growth dividend model)

Applies to companies that issue ordinary shares with dividend payments

Based on return on equity

Applies to companies that do not issue shares on the stock market, but with open financial statements (for example, for a closed joint stock company)

Based on risk premium

Used to assess the efficiency of equity capital of startups and venture businesses

Example No. 1. Calculation of WACC in Excel based on the CAPM model

Calculation of WACC for CJSC companies

Example No. 2. Calculation of WACC by balance in Excel

![]()

Modification of the WACC formula