The concept of markup and margin (people also say “gap”) similar to each other. They are easy to confuse. Therefore, first, let's clearly define the difference between these two important financial indicators.

We use markup to set prices, and margin to calculate net profit from total income. In absolute terms, the markup and margin are always the same, but in relative (percentage) terms they are always different.

Formulas for calculating margins and markups in Excel

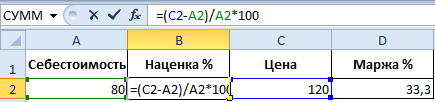

A simple example to calculate margin and markup. To implement this task, we need only two financial indicators: price and cost. We know the price and cost of the product, but we need to calculate the markup and margin.

Formula for calculating margin in Excel

Create a table in Excel, as shown in the figure:

In the cell under the word margin D2, enter the following formula:

As a result, we get the margin volume indicator, for us it was: 33.3%.

Formula for calculating markup in Excel

Move the cursor to cell B2, where the result of the calculations should be displayed, and enter the formula into it:

As a result, we obtain the following markup percentage: 50% (easy to check 80+50%=120).

The difference between margin and markup using an example

Both of these financial ratios consist of profits and expenses. What is the difference between markup and margin? And their differences are quite significant!

These two financial ratios differ in the way they are calculated and the results in percentage terms.

Markups allow businesses to cover costs and make a profit. Without it, trade and production would go into minus. And the margin is the result after the markup. For a clear example, let’s define all these concepts with the formulas:

- Product price = Cost + Markup.

- Margin is the difference between price and cost.

- Margin is the share of profit that the price contains, so the margin cannot be 100% or more, since any price also contains a share of the cost.

The markup is the part of the price that we added to the cost.

Margin is the portion of the price that remains after subtracting the cost.

For clarity, let’s translate the above into formulas:

- N=(Ct-S)/S*100;

- M=(Ct-S)/Ct*100.

Description of indicators:

- N – markup indicator;

- M – margin indicator;

- Ct – product price;

- S – cost.

If we calculate these two indicators in numbers then: Markup = Margin.

And if in percentage terms, then: Markup > Margin.

Please note that the markup can be as high as 20,000%, and the margin level can never exceed 99.9%. Otherwise, the cost will be = 0 rub.

All relative (percentage) financial indicators allow you to display their dynamic changes. Thus, changes in indicators in specific periods of time are monitored.

They are proportional: the higher the markup, the greater the margin and profit.

This gives us the opportunity to calculate the values of one indicator if we have the values of the second. For example, markup indicators allow you to predict real profit (margin). And vice versa. If the goal is to reach a certain profit, you need to figure out what markup to set that will lead to the desired result.

Let's summarize before practice:

- for margin we need indicators of sales amount and markup;

- For the markup we need the sales amount and the margin.

How to calculate the margin as a percentage if we know the markup?

For clarity, let's give a practical example. After collecting reporting data, the company received the following indicators:

- Sales volume = 1000

- Markup = 60%

- Based on the data obtained, we calculate the cost (1000 - x) / x = 60%

Hence x = 1000 / (1 + 60%) = 625

Calculate the margin:

- 1000 - 625 = 375

- 375 / 1000 * 100 = 37,5%

This example follows the formula for calculating margin for Excel:

How to calculate the markup as a percentage if we know the margin?

Sales reports for the previous period showed the following indicators:

- Sales volume = 1000

- Margin = 37.5%

- Based on the data obtained, we calculate the cost (1000 - x) / 1000 = 37.5%

Hence x = 625

We calculate the markup:

- 1000 - 625 = 375

- 375 / 625 * 100 = 60%

An example of an algorithm for calculating a markup formula for Excel:

Note. To check formulas, press the key combination CTRL+~ (the “~” key is located before the one) to switch to the corresponding mode. To exit this mode, press again.

29OctWhat is Margin

Margin is an indicator of product profitability, the difference between the cost of a product unit and the cost for which it is sold. It is measured in two quantities: absolute ( specific financial units, such as dollars) or the percentage of the difference between cost and value is applied to the market price of the product.

What is MARGIN - definition, meaning in simple words.

In simple words, margin is synonymous with commodity margin, profit received by a manufacturing company. The indicator can be calculated both from a specific unit of goods, and the gross margin can be calculated from total corporate income. But it is important to understand in more detail what margin is in business and trade, and how it differs from the same markup or profit.

What is margin in simple words and how to calculate it?

The word margin came into Russian from English, where financiers and economists use the word margin. But the French, whose language has the word marge, were the first to use such a term. Both words have varied semantics in their languages, ranging from the meaning of “stock” to the definitions of “profit” and “advantage”.

Margin is, in simple words, exactly the financial benefit that a businessman independently generates and then receives from the base cost of the product. This is precisely the price “margin” or “advantage”, which shows the profitability of the company.

What is margin? Formula and features of calculation

Let us more clearly demonstrate with an example what the term means and its difference between profit or product margin.

Margin calculation can be done in two ways:

- using absolute units ( specific dollars, euros, etc.);

- in relative percentage terms.

This is where confusion between markup and margin most often occurs. Let's take a simple example: the cost of a smartphone is $200, and its real market price is $300. The markup on this gadget is easy to calculate - $100. The margin indicator in absolute units of measurement will also be $100.

Strictly speaking, such a calculation is the first step in determining the cost-effective capabilities of a product. We have found out its absolute margin, and now we need to derive the percentage formula.

What margin is most relevant in the trade and financial sector?

So, for us now it is more relevant to calculate the margin in percentage terms. In the language of economists, this is called the “marginality coefficient,” which demonstrates the profitability of a specific unit of goods as a percentage.

It is calculated according to the formula: divide the profit from one commodity unit by the selling price and multiply by 100%. In previous calculations, we got an amount of $100 - our absolute margin. Divide 100 dollars by 300 ( total cost of goods) and multiply by 100 percent.

The margin ratio in our example is 33% ( rounded up). 33 percent is an indicator reflecting the product profitability of the conventional smartphone we gave as an example.

By the way, if we calculated the markup as a percentage, we would get a completely different number - 50%. With this example, we wanted to show how important it is to avoid confusion not only in terminology, but also in calculation formulas.

And one more small visualization. In previous calculations, we received a margin ratio of 33%. Relatively speaking, a company with this indicator receives 33 cents of profit for every dollar spent. The remaining 77 cents goes towards expenses.

What is gross margin?

If in the previous examples we focused on the margin coefficient of a specific unit of goods, then the gross margin is the residual amount of income of the enterprise after deducting variable costs. The latter include:

- raw materials purchase of production materials;

- payment of wages to workers;

- expenses;

- transportation costs, etc.

In European terminology you can find the term grossprofit ( or grossmargin), defining this indicator. Europeans, unlike many CIS countries, calculate percentages rather than absolute values. Very often, this causes confusion and discrepancies in the interpretation of financial accounting documentation.

Gross margin will never be a real reflection of the financial condition of the company, but it allows you to see the real picture: how the company manages to cope with the sale of goods, reducing or increasing variable costs. In addition, this indicator makes it possible to calculate other, more important criteria for the operation of the enterprise.

What is margin in banking?

The term "margin" is also used in the banking sector. Financiers analyze the activities of a particular bank, simultaneously calculating four types of margin indicators:

- banking: the difference between lending rates and deposits made is calculated;

- credit: the difference between two amounts – defined in the contract and actually issued to the client;

- warranty: calculated by subtracting the collateral amount from the loan volume;

- net margin: calculated as a percentage using the formula - commission expenses are subtracted from commission income and the resulting result is divided by bank assets.

The last formula is decisive in demonstrating the success or failure of a particular bank. The calculation can take into account not only all total banking assets, but also only those that actually operate at the moment ( make a profit).

Categories: , // fromIn the economic sphere, there are many concepts that people rarely encounter in everyday life. Sometimes we come across them while listening to economic news or reading a newspaper, but we only imagine the general meaning. If you have just started your entrepreneurial activity, you will have to familiarize yourself with them in more detail in order to correctly draw up a business plan and easily understand what your partners are talking about. One such term is the word margin.

In trade "Margin" expressed as the ratio of sales proceeds to the cost of the product sold. This is a percentage indicator, it shows your profit when selling. Net profit is calculated based on margin indicators. It’s very easy to find out the margin indicator

Margin=Profit/Sales Price * 100%

For example, you bought a product for 80 rubles, and the selling price was 100. The profit is 20 rubles. Let's do the calculation

20/100*100%=20%.

The margin was 20%. If you have to work with European colleagues, it is worth considering that in the West the margin is calculated differently than in our country. The formula is the same, but net income is used instead of sales proceeds.

This word is widespread not only in trade, but also on stock exchanges and among bankers. In these industries, it means the difference in securities prices and the bank’s net profit, the difference in interest rates on deposits and loans. For different areas of the economy, there are different types of margin.

Margin at the enterprise

The term gross margin is used in businesses. It means the difference between profit and variable costs. It is used to calculate net income. Variable costs include equipment maintenance costs, labor costs, and utilities. If we are talking about production, then gross margin is the product of labor. It also includes non-operating services that are profitable from outside. This is an identifier of a company's profitability. From it various monetary bases are formed to expand and improve production.

Margin in banking

Credit margin– the difference between the commodity value and the amount allocated by the bank for its purchase. For example, you take out a table worth 1000 rubles on credit for a year. After a year, you pay back 1,500 rubles in total with interest. Based on the formula above, the margin on your loan for the bank will be 33%. Credit margin indicators for the bank as a whole affect the interest rate on loans.

Banking– the difference between the interest rate coefficients on deposits and issued loans. The higher the interest rate on loans and the lower the interest rate on deposits, the greater the bank margin.

Net interest– the difference between interest income and expense in a bank in relation to its assets. In other words, we subtract the bank's expenses (paid loans) from income (profit on deposits) and divide by the amount of deposits. This indicator is the main one when calculating the bank’s profitability. It defines stability and is freely available to interested investors.

Warranty– the difference between the probable value of the collateral and the loan issued against it. Determines the level of profitability in case of non-return of money.

Margin on the exchange

Among traders participating in exchange trading, the concept of variation margin is widespread. This is the difference between the prices of the purchased futures in the morning and in the evening. A trader buys futures for a certain amount in the morning at the beginning of trading, and in the evening, when trading closes, the morning price is compared with the evening price. If the price has increased, the margin is positive; if it has decreased, the margin is negative. It is taken into account daily. If analysis is needed over several days, the indicators are added up and the average value is found.

The difference between margin and net income

Indicators such as margin and net income are often confused. To feel the difference, you should first understand that margin is the difference between the values of purchased and sold goods, and net income is the amount from sales minus consumables: rent, equipment maintenance, utility bills, wages, etc. If we subtract the tax from the resulting amount, we get the concept of net profit.

Margin trading is a method of buying and selling futures using borrowed funds against certain collateral - margin.

The difference between margin and “cheat”

The difference between these concepts is that the margin is the difference between the sales profit and the cost of the goods sold, and the markup is the profit and the cost of the purchase.

In conclusion, I would like to say that the concept of margin is very common in the economic sphere, but depending on the specific case, it affects different indicators of the profitability of an enterprise, bank or stock exchange.

a term denoting the difference between the prices of goods, interest rates, exchange rates and securities; margin is also an indicator of the activity of an enterprise, which is used in marginal analysis

Information about the concept of margin, the use of the term “margin” in stock exchange, banking, insurance, trading and bookmaking activities, calculation of margin, calculation of marginal income and the difference between margin and markup, margin trading and types of margin when trading on the exchange

Expand contents

Collapse content

Margin is the definition

Margin is a concept denoting the difference between the price of a product and its cost, and expressed in absolute values. Margin also refers to the size of the required advance when trading on the stock exchange, and the difference between loan rates and interest rates in banking. In general market terminology, the concept of margin refers to the difference between indicators specific to each type of activity.

Margin is a term used in trading, exchange, insurance and banking practice to denote the difference between the prices of goods, securities rates, interest rates and other indicators.

Margin concept

Margin is the difference between price and cost (analogous to the concept of profit). It can be expressed both in absolute values (for example, rubles) and as a percentage, as the ratio of the difference between price and cost to price (in contrast to the trade margin, which is calculated as the same difference in relation to cost).

Margin is a pledge that provides the opportunity to obtain a temporary loan of money or goods that are used to carry out speculative stock exchange transactions during margin trading. A marginal loan differs from a simple loan in that the amount of money received (or the cost of the goods received) usually exceeds the amount of collateral (margin). Typically, margin (margin requirement) is expressed as a percentage (%), as the ratio of the collateral amount to the transaction amount (for example, 25%) or as a ratio of shares (for example, 1:4). In spread betting, the margin can be 3-5%, which allows you to increase both winnings and losses.

Margin is the difference between the selling price and the cost. This difference is usually expressed either as a percentage of the selling price (profitability ratio) or in absolute terms as profit per unit of production.

Margin is the difference between the selling price of a commodity unit and the cost of a commodity unit. This difference is usually expressed as profit per unit or as a percentage of the selling price (profitability ratio). In general, margin is a term used in trading, stock exchange, insurance and banking practice to denote the difference between two indicators.

Margin is the percentage of the cost of goods that must be added to their cost to arrive at the selling price.

Margin is the difference between the selling and purchasing prices of securities by a market maker or goods by a dealer. In informal vocabulary, this process is often called “haircut”.

Margin is the price added to or subtracted from the market interest rate on a deposit to ensure that the bank makes a profit.

Margin and business

Margin is the amount of advance made to a broker or dealer by a trader or investor when purchasing futures.

Margin is money or securities deposited with a stockbroker to cover a client's potential losses.

Margin is a term used in trading, exchange, insurance and banking practice to denote the difference between the prices of goods, securities rates, interest rates, and other indicators.

Margin is- in general market terminology - the difference between price and cost.

Working with margin

Margin is- in marketing - a trade margin established by industrial enterprises.

Margin is- in futures stock transactions - the difference between the security rate on the day of conclusion and the day of execution of the transaction or the difference between the buyer and seller prices.

Margin is the amount of collateral that is necessary for traders to maintain open positions in the Forex market.

Margin is a definition that came to e-commerce from the field of finance and banking.

Margin is the difference between product prices is essentially the profitability of sales.

Margin is the difference between interest rates, loan rates, securities rates, purchase and sale prices of goods and other indicators, the value of which determines the profit received by companies, firms, individual entrepreneurs buying and selling these goods, securities, financial assets, etc. d.

Margin is the difference between credit and deposit interest rates; between rates on loans provided to different categories of borrowers; between the amount of collateral against which the loan was granted and the amount of the loan issued.

Margin is a term used in banking, stock exchange, and trade insurance practice to denote the difference between interest rates, securities rates, commodity prices and other indicators; the difference between the rates on attracted and provided loans; between rates on loans provided to different categories of borrowers; the amount of collateral against which the loan was provided and the amount of the loan issued; additional share of the deposit, collateral or permissible fluctuations in the exchange rate.

Margin is the difference between securities rates, interest rates, commodity prices and other industry-specific indicators.

In a general sense, margin refers to the difference in product prices, stock exchange quotes, interest rates, etc. The term has become widespread in many areas: trading, banking, stock exchange, insurance, etc. and has quite a lot of nuances in its definition.

For example, in general economic theory, margin is the difference between the price of a product and its cost.

When analyzing the activities of an enterprise, the economist-analyst is interested in the gross margin - the difference between the company's revenue from the sale of products and variable costs, that is, those that change in direct proportion to the volume of products produced. The size of the gross margin directly affects net profit and it is from it that development funds are formed (more about this in the article “what is capital”). There is also a gross margin coefficient, calculated as the ratio between the gross margin and the amount of revenue from the sale of a batch of goods. At the same time, it is important to assess the level of marginal income received by the company. It can be calculated either as gross margin or as the sum of fixed costs and profit. The rate of marginal income is understood as the share of marginal income in the company’s total revenue from sales of goods.

There is also a concept similar to gross margin, such as “profit margin,” which means the share of profit in the total trading capital, and simply put, it determines the profitability of sales.

In the banking sector, such concepts as credit margin are applicable - that is, the difference between the amount of goods fixed in the loan agreement and the actual amount issued to the borrower.

And if we talk about the sources of profit of a banking organization, then it will largely be determined by the size of the bank margin - the difference between interest rates on loans and deposits. Or the so-called net interest margin is better suited for these purposes - the difference between the bank’s net interest income (obtained through lending and investing) and the rate paid on capital and liabilities.

It is appropriate to talk about margin when it comes to a secured loan - in this case it will be the so-called guarantee margin - the difference between the value of the collateral and the size of the loan issued.

Margin calculation

Margin (return on sales) is the difference between the selling price and the cost. This difference is usually expressed either as a percentage of the selling price or as profit per unit. Margin calculation (formula):

The purpose of the margin is to determine the amount of sales growth and manage pricing and decision-making on product promotion.

Margin and price

The return on sales threshold is a key factor among many other basic types of business calculations, including estimates and forecasts. All managers should (and usually do) know their company's estimated return on sales and what it represents. However, managers vary greatly in the assumptions they use to calculate return on sales and in the ways they analyze and know what margins are.

When talking about margin, it is important to keep in mind the difference between profitability ratio and profit per unit on sales. This difference is easy to reconcile, and managers must be able to switch from one to the other.

What is a unit of production? Each company has its own idea of what a unit of production is, which can range from a ton of margarine to 1 liter of cola or a bucket of plaster. Many industries deal with numerous units of output and calculate commercial margins accordingly. In the tobacco industry, for example, cigarettes are sold in pieces, packs, blocks and boxes (which hold 1,200 cigarettes). In banks, margin is calculated based on accounts, customers, loans, transactions, family units and bank branches. You must be able to easily switch from one concept to another, since decisions can be based on any of them.

The profitability ratio can also be calculated using gross sales in monetary terms and total costs.

When calculating return on sales, expressed both as a percentage (profitability ratio) and as profit per unit, a simple reconciliation can be performed by checking whether the individual parts add up to the total.

Markup or margin?

Although some people characterize the terms "margin" and "markup" as interchangeable concepts, this is not true. The term markup usually refers to the practice of adding a certain percentage to the cost to calculate selling prices.

As you know, any trading company lives off the markup, which is necessary to cover costs and make a profit:

What is margin, why is it needed and how does it differ from markup, if it is known that margin is the difference between the selling price and cost?

It turns out that this is the same amount.

Margin and markup

What's the difference?

The difference lies in the calculation of these indicators in percentage terms (the markup refers to the cost, the margin refers to the price).

It turns out that in digital terms the amount of markup and margin are equal, but in percentage terms the markup is always greater than the margin.

For example:

It is interesting to note here that the margin cannot be equal to 100% (unlike the markup), because in this case, the Cost should be equal to zero, which, as we know, does not happen, although we would really like it!

The concepts of margin and markup

Like all relative (expressed as a percentage) indicators, markup and margin help to see processes in dynamics. With their help, you can track how the situation changes from period to period.

Looking at the table, we clearly see that the markup and margin are directly proportional: the higher the markup, the greater the margin, and therefore the profit.

The interdependence of these indicators makes it possible to calculate one indicator given the second. Thus, if a company wants to reach a certain level of profit (margin), it needs to calculate the markup on the product, which will allow it to obtain this profit.

In order not to get confused once again, learn the rule that margin is the ratio of profit to PRICE (i.e. the percentage of profit in the price of a product), and the markup is the ratio of profit to COST (i.e. the percentage of profit in the cost ).

Gross Margin

Gross margin is one of the most important indicators of operational analysis, which is widely used in financial management and controlling.

Gross margin is the difference between the total revenue from sales of products and the variable costs of the enterprise. Gross margin refers to estimates. By itself, the gross margin indicator does not allow us to assess the overall financial condition of the enterprise or a specific aspect of its activities. The “gross margin” indicator is used to calculate a number of other indicators. For example, the ratio of gross margin and revenue is called the gross margin ratio.

Gross margin is the basis for determining the net profit of an enterprise; company development funds are formed from the gross margin. Gross margin is an analytical indicator that characterizes the performance of the enterprise as a whole.

The gross margin is created due to the labor of the enterprise’s employees invested in the production of goods (rendering services). Gross margin expresses the surplus product created by the enterprise in monetary form. The gross margin may also take into account income from the so-called non-operating economic activities of the enterprise. Non-operating income includes the balance of transactions for non-industrial services, housing and communal services, write-off of receivables and payables, etc.

Gross margin represents the share of each ruble in sales that the company retains as gross profit. For example, if a company's gross margin for the last quarter was 35%, that would mean it retained R0.35. from each ruble received as a result of sales to be used to pay off commercial, general and administrative expenses, interest expenses and payments to shareholders. Gross profit levels can vary significantly from one trade to another.

There is an inverse relationship between gross margin and inventory turnover: the lower the inventory turnover, the higher the gross margin; The higher the inventory turnover, the lower the gross margin. Manufacturers must ensure higher gross margins than trade because their product spends more time in the production process. Gross margin is determined by pricing policy.

Gross margin is calculated using the following formula:

Gross Margin Ratio

The gross margin ratio is the ratio of gross profit to revenue. In other words, it shows how much profit we will get from one dollar of revenue. If the gross margin ratio is 20%, this means that every dollar will bring us 20 cents of profit, and the rest must be spent on producing the product.

Let us recall that the gross margin, by definition, is designed to cover the costs associated with the general management of the company and the sale of finished products, and, in addition, provide it with profit. In this sense, the gross margin ratio shows the ability of the company's management to control production costs (the cost of raw materials and direct materials, direct labor costs and production overhead costs). The higher this indicator, the more successfully the company's management manages production costs.

Gross margin in Russia

In Russia, gross margin is understood as the difference between an enterprise’s revenue from sales of products and variable costs.

However, this is nothing more than marginal income, contribution margin - the difference between revenue from product sales and variable costs. Gross margin is a calculated indicator that does not in itself characterize the financial condition of the enterprise or any aspect of it, but is used in the calculation of a number of financial indicators. The amount of marginal income shows the enterprise’s contribution to covering fixed costs and making a profit.

Gross margin in Europe

There are differences in the understanding of gross margin that exist in Europe and the concept of margin that exists in Russia. In Europe (more precisely, in the European accounting system) there is the concept of Gross margin. Gross margin is the percentage of total sales revenue that a company leaves after incurring direct costs associated with the production of the goods and services sold by the company. Gross margin is calculated as a percentage. These differences are fundamental to the accounting system. Thus, Europeans calculate gross margin as a percentage, while in Russia “margin” is understood as profit.

Margin analysis

A major role in justifying management decisions in business is played by marginal (marginal) analysis, the methodology of which is based on studying the relationship between three groups of the most important economic indicators: “costs - volume of production (sales) of products - profit” and predicting the critical and optimal value of each of these indicators for a given value of others. This method of management calculations is also called break-even or income assistance analysis.

The essence of marginal analysis is to analyze the ratio of sales volume (product output), cost and profit based on forecasting the level of these values under given restrictions.

Marginal analysis serves to find the most profitable combinations between variable costs per unit of production, fixed costs, price and sales volume. Therefore, this analysis is impossible without dividing costs into fixed and variable.

The values of specific marginal income for each specific type of product are important for the manager. If this indicator is negative, then the revenue from the sale of the product does not even cover variable costs. The calculation of marginal income allows you to determine the impact of production and sales volume on the amount of profit from the sale of products, works, services and the sales volume from which the company makes a profit.

The basis of marginal analysis is the division of costs into variable and fixed.

In practice, the set of criteria for classifying an item as a variable or constant part depends on the specifics of the organization, the adopted accounting policy, the goals of the analysis and the professionalism of the relevant specialist.

Practice shows that, as a rule, enterprises in the industry are not limited to single-item production, and therefore, there is a need to conduct marginal analysis in conditions of multi-item production.

Marginal analysis of activities

Due to the fact that different types of products are sold at different prices, have different costs and profit margins for multi-item production, marginal analysis becomes more complicated. This problem can be solved in various ways, including a separate analysis of the product range with the determination of individual break-even points using the equation that is used when analyzing a single product. In this case, it is advisable, along with direct variable costs, to attribute direct fixed costs directly to a specific type of product (which clearly relate to this type of product and disappear when its production is discontinued).

The result of a break-even analysis largely depends on the cost structure, i.e., on the ratio of variable and fixed components in total costs. The theory of marginal analysis does not give a clear answer to the question of what should be the most optimal (profitable) ratio of variable and fixed costs.

With high fixed costs, reaching the break-even point requires a significant volume of sales, which can be associated with a long period of time. The positive aspect is high profit growth after reaching the break-even point. However, organizations with these characteristics pose high risks.

Organizations with low fixed costs and high variable costs receive more stable profits and are less risky.

Minimizing business risks can be facilitated by transferring part of the fixed costs to the category of variable ones. Sometimes an enterprise has this opportunity by replacing time-based wages for the main workers with a piece-rate form of remuneration, linking the wages of the enterprise’s sales departments to sales volumes, etc.

With the same amount of costs, reducing the share of fixed costs in it has a beneficial effect on the financial stability of the enterprise: the value of the break-even point and the strength of the operating leverage are reduced, and the margin of financial strength increases. At the same time, production risks are reduced, but the enterprise’s activities become less efficient.

It is quite difficult to give a definite answer as to which option for the ratio of fixed and variable costs is better. Often, a technological process requires that fixed costs be high and variable costs low, in which case, when high production volumes and stable sales are achieved, high profits become possible.

Margin analysis (break-even analysis) allows you to:

To more accurately calculate the influence of factors on changes in the cost of products (services), the amount of profit, the level of profitability and, on this basis, more effectively manage the process of forming and forecasting costs and financial results;

Determine critical levels of sales volume, variable costs per unit of production, fixed costs, prices at a given value of the relevant factors;

Establish the safety zone (break-even) of the enterprise and assess the degree of its sensitivity to changes in external and internal factors;

Calculate the required sales volume to obtain a given amount of profit;

Justify the most optimal option for management decisions regarding changes in production capacity, product range, pricing policy, equipment options, production technology, acquisition of components and others in order to minimize costs and increase profits.

The most important disadvantage of using marginal analysis is the conditional nature of the division of costs into fixed and variable components, which entails inaccuracy of the results obtained. In addition, with multi-item production, the problem of dividing general variable costs between individual types of products arises.

Significantly complicating the marginal analysis is the lack of breakdown of costs as part of overhead expenses in Form 2 “Profit and Loss Statement” into constant and variable components, and therefore there is a need to use one of the methods existing in the theory of economic analysis to solve this problem, for example :

Statistical correlation method (graphical);

Highest and lowest point method;

Least square method.

Another disadvantage of using marginal analysis is the problem of distributing indirect fixed costs related to the activities of the organization as a whole.

Perhaps it makes sense when analyzing each specific product not to distribute indirect costs, but to plan production based on the optimal structural distribution of products with further analysis of the sufficiency of the revenue received to cover fixed costs.

The second possible solution may be the development of the previous option, i.e., the optimal structure of the ratio of manufactured products in the total volume of output is taken as a conditional single product (a package of a multi-product output). The price of the package and variable costs are determined in a share ratio; fixed costs are known. A significant drawback of the method: the structure of the package is considered unchanged, which is unlikely in the modern market. A possible solution is to conduct an analysis for several of the most likely share ratios of products in the package, taking into account possible changes in pricing policy, expansion of production space, etc.

The main category of marginal analysis is marginal income. Marginal income (profit) is the difference between sales revenue (excluding VAT and excise taxes) and variable costs.

Sometimes marginal income is also called the coverage amount - this is the part of the revenue that remains to cover fixed costs and generate profit. The higher the level of marginal income, the faster fixed costs are recovered and the organization has the opportunity to make a profit.

Marginal analysis of an enterprise allows the entrepreneur and the management of the enterprise to reliably assess the current situation and prospects. He must answer the question: what are the sources and amounts of funds that the company has, and for what purposes and needs is it spent?

The analysis evaluates the efficiency of using monetary resources and capital. A mandatory section of the analysis is the study of the composition and sources of income and directions of expenses of the company, consideration of sales volumes of goods and services, cost of products sold, highlighting gross, fixed and variable costs. Profit and profitability indicators must be identified and assessed, and trends in their dynamics must be identified.

Marginal income

The term marginal income (MI), from English. marginal revenue, used in two meanings:

Marginal income is additional income received from the sale of an additional unit of goods;

Income received from sales after reimbursement of variable costs. In this case, marginal income is the source of profit generation and covering fixed costs.

This discrepancy is due to the polysemy of the English word marginal:

Ultimate, this is where the words “marginal, marginal” come from - located on the border, at the limit of the generally accepted;

Change, difference, this is where the word “margin” comes from - the difference in interest rates, etc.

Thus, marginal income is fixed costs and profit. Often, instead of marginal income, the term “covering contribution” is used: marginal income is a contribution to cover fixed costs and generate net profit.

The formula for calculating marginal income does not show its dependence on fixed costs, variable costs and price. But in the examples of calculating marginal income it is clear that this dependence exists.

Marginal income is especially interesting if the enterprise produces several types of products and it is necessary to compare which type of product makes a greater contribution to total income. To do this, calculate what part the marginal income is in the share of revenue (income) for each type of product or product.

Margin in exchange activities

The profit of exchange trading participants depends on the difference between the sale and purchase prices of the exchange commodity, which are indicated in the exchange bulletin. In a broader sense, in exchange practice, the term “margin” is used to refer to the difference between securities rates.

Margin trading is carrying out speculative trading operations using money and/or goods provided to the merchant on credit secured by an agreed amount - margin. A margin loan differs from a simple loan in that the amount of money received (or the cost of the goods received) is usually several times greater than the amount of collateral (margin). For example, for granting the right to conclude a contract for the purchase or sale of 100 thousand euros for US dollars, a broker usually requires no more than 2 thousand dollars as collateral. This allows the trader to increase the volume of transactions with the same capital. In addition, with margin trading, it is usually allowed to sell goods taken on credit with the expected subsequent purchase of a similar product and repayment of the loan in kind (commodity). This operation is called a short position or short sale (uncovered sale). This mechanism provides the technical ability to make a profit when prices fall (examples are given below).

The margin principle is widely used in exchange trading of any instruments.

About margin trading

Margin trading involves performing transactions with assets received from a broker on credit. This can be either cash or traded goods: for example, shares, futures contracts. Margin lending has its own specifics. Usually the following conditions are stipulated:

Obtaining a loan does not require prior approval or specific registration;

The loan is secured by cash and other assets placed in the relevant accounts;

The loan is provided by assets from the list of assets with which margin transactions can be made;

Credits during the trading session are provided free of charge;

In many cases, such as stock trading, there is a fee for extending credit for more than a day. This is usually an agreed upon percentage of the loan amount or the market value of the loaned assets. Typically, the interest rate depends on the type of loaned asset and is focused on existing interest rates for similar transactions in “regular” interbank lending.

The size of margin requirements greatly depends on the liquidity of the commodity being traded. In the foreign exchange market, the margin is usually 0.5-2%. On weekends it can rise to 5-10%. In the USA, Great Britain, Germany, the margin on the stock market can be 20-50%. In Russia, for trading in some stocks for some traders, the Federal Service for Financial Markets (until 2004 its functions were performed by the Federal Commission for the Securities Market) allows a margin of 25 - 50% of the contract amount (as of February 2007). The size of the margin may depend on the direction of the first transaction (buy or sell).

About margin trading in derivatives

Regulatory authorities in crisis situations additionally limit the possibility of conducting margin transactions. To combat the panic and rumors that gripped Wall Street, the Securities and Exchange Commission urgently limited short selling of securities of 19 large financial companies from July 21, 2008, and from September 19, 2008, this list expanded to 799 financial companies. The UK Financial Services Authority (FSA) has imposed a temporary ban on short selling shares on the London Stock Exchange from 19 September 2008 until 16 January 2009.

On September 17, 2008, the Federal Service for Financial Markets of Russia suspended trading in all securities on Russian stock exchanges. In a commentary by the head of the Federal Financial Markets Service of Russia, Vladimir Milovidov, this step is explained by the fact that “brokers continue to enter into margin transactions and open short positions, further destabilizing the situation.”

The concept of margin trading

Margin trading always assumes that the trader will definitely carry out an opposite operation for the same volume of goods after some time. If the first was a purchase, then a sale will certainly follow. If the first was a sale, then a purchase is definitely expected. After the first operation (opening a position), the trader is usually deprived of the opportunity to freely dispose of the purchased product or the funds received from the sale. He also pledges part of his own funds in the amount of the agreed margin as collateral. The broker closely monitors open positions and controls the size of the possible loss. If the loss reaches a critical value (for example, half the margin), the broker may contact the trader with a proposal to pledge additional funds. This call is called a margin call - from the English. Margin call (literal translation - margin requirement). If funds are not received and the loss continues to increase, the broker will forcefully close the position on its behalf. After the second operation (closing a position), a financial result is generated in the amount of the difference between the purchase price and the sale price, and the collateral margin is released, to which the result of the operation is added. If the result is positive, the merchant will receive back more money in the amount of profit than he pledged. If the result is negative, the loss will be deducted from the deposit and only the remainder will be returned. In the worst case scenario, there will be nothing left of the collateral.

The trader does not have any additional financial obligations to the broker for the loan received, other than providing margin. Typically, a broker cannot make a demand for additional funds on the basis that a position was closed at a loss that exceeded the amount of collateral provided. This situation can occur at the opening of a new trading day, when trading begins with a strong gap from the quotes of the previous day. In this case, the risk of additional losses lies with the broker. This is the fundamental difference between margin trading and trading using conventional credit. In this way, margin trading is similar to gambling, where the risk is usually limited by the size of the bet.

Margin trading on the foreign exchange market

To be able to carry out margin trading, the broker usually does not provide the trader with full ownership of the instruments being traded or requires the execution of a special collateral agreement. The trader should not be able to prevent the broker from forcing positions to close out. Very often, the goods and/or proceeds from the sale are not transferred to the ownership of the merchant at all. Only his right to give an order to buy/sell is taken into account. As a rule, this is enough for transactions of a speculative nature, when the trader is not interested in the object of trade, but only in the opportunity to make money on the difference in price. This type of trading without actual delivery reduces the speculator's overhead costs.

To quickly determine intermediate profit, the price of a point is usually calculated - the change in the result with a minimal change in the quote (by one point). Subsequently, the price of the point is simply multiplied by the number of points of change in the quote.

What is margin trading

Alternative names for margin trading

There are other names for margin trading.

Trading with leverage

Leverage is the ratio between the amount of collateral and the borrowed capital allocated for it. Instead of indicating the size of the margin, indicate the size of the leverage (leverage) in the form of a coefficient that shows the ratio of the amount of collateral to the size of the loan provided. For example, a margin requirement of 20% corresponds to a leverage of 1:5 (one to five), and a margin requirement of 1% corresponds to a leverage of 1:100 (one to one hundred). In this case, the trader is said to receive 5 (or 100) times more funds for trading than the amount of his security deposit.

Trade without delivery

This term emphasizes the specific feature of this type of operation, but does not give an idea of the actual trading conditions.

The benefits of margin trading

Benefits of margin trading for a trader:

Allows the trader to repeatedly increase the volume of transactions without increasing the amount of required capital;

Allows a trader to conduct transactions in capital-intensive markets even without having their own significant amounts of money;

Provides the technical ability to make a profit when prices fall.

Benefits of margin trading for a broker:

Additional income in the form of interest payments for using the loan. Interest on a margin loan is often significantly higher than interest on bank deposits (it is more profitable for a broker to use funds for margin lending to clients than to place funds on bank deposits);

The client makes transactions for a larger volume, which leads to an increase in broker commissions, including in the form of spreads for broker-market makers;

The broker expands the circle of potential clients by lowering the minimum capital threshold sufficient to carry out transactions.

Risks of margin trading

The widespread use of margin trading increases the number and amount of transactions in the market. This leads to an increase in the rate of change in the result of a trading operation and to an increase in risks. An increase in transaction volumes affects the nature of the market. A large number of chaotic small transactions increases the liquidity of the market and stabilizes it. On the other hand, if trades are unidirectional, they can significantly increase price fluctuations.

Using leverage proportionally increases the speed of generating income when the price moves towards an open position. However, if the price moves in the opposite direction, the rate of increase in losses increases to exactly the same extent. This can lead to both very rapid enrichment and rapid loss of capital. To find the optimal amount of leverage used, you need to pay attention to the average volatility of quotes for the instrument being traded. The higher the volatility, the higher the likelihood that the use of high leverage can lead to significant losses even from random market fluctuations.

Securities margin

For securities, the concept of margin is formed by three important components: margin loan, margin deposit and margin requirement. A margin loan is the amount of money an investor borrows from his broker to purchase securities. A margin deposit is the amount of capital contributed by an investor to purchase securities in a margin account. The margin requirement is the minimum amount that the client must deposit, usually expressed as a percentage of the current market value. The size of the margin deposit can be greater than or equal to the margin requirement.

Borrowing money to purchase securities is called “buying on margin” (purchase “on margin” or purchase with payment of part of the amount using a loan). When an investor borrows money from his broker to buy a stock, he is required to open a margin account with the broker, sign an appropriate agreement, and follow the broker's margin requirements. The credit on the account is secured by the investor's securities and money. If the share price drops significantly, the investor will need to deposit additional funds into the account or sell part of the shares.

The Federal Reserve Board and self-regulatory organizations such as the New York Stock Exchange and FINRA set clear rules for margin trading. In the US, Regulation T allows investors to borrow up to 50 percent of the value of securities purchased on margin. The percentage of the purchase price of securities that an investor must pay is called the initial margin. To purchase securities on margin, an investor must first deposit a specified amount of cash or broker-qualified securities that will be sufficient to meet the initial margin requirement for the purchase.

According to NYSE and FINRA rules, after an investor purchases shares on margin, the client's margin account must maintain a specified minimum amount of funds. These rules stipulate that investors must have funds in their account, the amount of which is at least 25 percent of the market value of the securities they own. This is called the "maintenance margin". For market participants classified as Pattern Day Traders, the minimum margin requirement is $25,000 or 25% of the total market value of the securities, whichever is greater.

If the margin account balance falls below the minimum requirements, the broker has the right to liquidate the position or require the investor to increase the amount of collateral, i.e. depositing additional funds.

Brokers also set their own minimum margin requirements, the so-called. "local" requirements (house requirements). Some brokers have more lenient lending terms than others, which may also vary from client to client. Despite this, brokers are required to conduct their activities in accordance with the established requirements of regulatory organizations.

Not all securities can be purchased on margin. Buying on margin is a double-edged sword. As a result of such trading, you can either make big profits or suffer big losses. In a volatile market, investors who have borrowed money from their brokers may need to deposit additional funds if the stock price drops significantly (if buying on margin) or rises too much (if shorting the stock). In such cases, brokers have the right to liquidate a position without even informing the investor. It is extremely important when shorting stocks and buying on margin to monitor your positions in real time.

Commodity Margin

Commodity margin is the amount of money invested by an investor to maintain a futures contract.

Margin requirements for futures or futures options are set by each exchange through a calculation algorithm known as "SPAN margining". SPAN (Standard Portfolio Analysis of Risk) evaluates the overall risk of a portfolio by calculating the largest possible losses that the derivatives and physical instruments contained in a given portfolio could result in over a specified time interval (usually one trading day). Valuation occurs by calculating profits and losses under different market conditions. The most important part of the SPAN methodology is the SPAN Risk Array, which is a set of numeric values that represent increases and decreases in the value of a particular contract under various conditions. Each condition is called a risk scenario. The numerical value of each risk scenario reflects the gain and loss in contract value under various combinations of price (or underlying price) changes, volatility, and approach to expiration.

Like securities, commodities have initial and minimum margin requirements. These requirements are typically set by individual exchanges and are a percentage of the current value of the futures contract, determined based on the volatility and price of the contract. The initial margin requirement for a futures contract is the amount of money that must be posted as collateral to open a position in the contract. In order to buy a futures contract, you need to meet the initial margin requirement, that is, transfer or already have the required amount of funds in your account.

The minimum margin for commodities is the amount of funds that must be maintained in an account to maintain a position in a futures contract. It represents the minimum level of account balance to which you can drop without the need to deposit additional funds. Items are marked to market daily and your account is adjusted for any resulting gains or losses. Because underlying commodity prices vary, there is a possibility that the value of a commodity could decline to a level that would cause your account balance to fall below minimum margin requirements. If this happens, the broker will most likely require an increase in the amount of collateral (margin call). In this case, you will have to deposit additional funds to meet the margin requirement.

Initial Margin

Initial margin is the amount of money that must be on the client's trading account in order for him to open a position. If there is less money in the account than the specified level, a futures transaction cannot be completed. This amount is indicated for one futures contract; it must be multiplied by their number in the transaction. The profit received from changes in the price of these contracts is added to the client's account balance at the end of the trading day. Likewise, the loss is deducted from it, but only until a certain level is reached.

About Initial Margin

Maintenance Margin

Maintenance margin is the same level of funds below which a trading account cannot fall if there are open positions on it. If a client incurs losses as a result of price changes on the exchange, the amount in his account may fall below the maintenance margin level. The same situation may arise if the margin levels were raised by the exchange, and there was not enough free money in the account to meet the new requirements. In this case, the client receives a call from the broker, who informs him about a lack of funds. This message from the broker is known among traders as a “margin call.” This situation can be resolved in two ways - either add additional funds to the trading account, or close part of the existing positions in order to free up part of the funds used as margin collateral. If the client does not take any action within the established time frame, the broker can protect himself by independently closing client positions at prices available on the market.

The concept of maintenance margin

Quoted Margin

Quoted margin is the difference between two yield levels or between a benchmark index and the price of a stock.

Additional Margin

Additional margin refers to the obligation to provide additional collateral.

Margin calls are one option where brokers require additional cash or collateral when their securities become partially worthless.

Deposit margin

Deposit margin is an instrument used in leveraged trading on futures exchanges. The “leverage effect” is explained by the fact that to purchase a futures contract, you only need to have in your brokerage account an amount corresponding to the collateral (GB), that is, 1-20% of the value of the underlying asset. This amount, frozen in your account when you open positions, is called deposit margin. You can buy futures on it with a total value of 5-100 times the contents of your deposit account.

The Exchange has the right to change the collateral rates (GS). It is interesting to note that this may affect the value of the contracts themselves on the exchange. Thus, an increase in the GO rate can lead to a decrease in the value of the futures contract. This happens due to a lack of funds to cover the deposit margin of small market participants. They begin to close positions, which leads to an avalanche decline in prices.

Variation margin

Variation margin is the amount paid/received by a bank or a participant in trading on an exchange in connection with a change in the monetary obligation for one position as a result of its adjustment by the market.

For futures contracts, variation margin is determined in the following order:

On the day of concluding a futures contract - as the difference between the price at which this contract was concluded and the settlement price of the corresponding futures contracts, resulting from the results of trading at the end of the day of its conclusion;

On the day between the day of conclusion and the day of termination of the futures contract - as the difference between the previous settlement price of the relevant futures contracts and the last settlement price;

On the day of termination of the futures contract - as the difference between the previous settlement price of the relevant futures contracts and the price at which the contract is terminated.

What is variation margin

Variation margin on the stock exchange is a concept that relates primarily to futures trading. In this case, it is called variational because of constant change. It is calculated from the moment the position is opened. Let's say we bought a futures contract on the RTS index at a price of 150,100 points, and ten minutes later the price rose to 150,200 points. In this case, the size of the variation margin was 100 points, but, naturally, this parameter is measured not in points, but in rubles (that is, approximately 67 rubles). If we do not take profit, but simply continue to keep the position open, then at the end of the trading session (that is, in the evening clearing), the variation margin goes to the accumulated income column and on the new trading day, the margin will begin to accrue again.

Simply put, if we kept the position open for one trading session, then the profit and loss on the transaction will be equal to the margin value, and if the position was open for several sessions, then its result is the sum of the margin values for each day. A positive margin value indicates profit on a given time interval (that is, we have correctly determined the direction of price movement), a negative margin indicates losses on our trading account.

Determination of variation margin

Forward margin

Forward margin is the difference (discount or premium) between the exchange rate for cash transactions (spot) and for term transactions. The forward margin is based on the rule of interest parity, which states that the forward rate tends to be as many points above the spot rate as the percentage rate in one currency is lower than the interest rate in the other currency, and vice versa.

Forward margins, like exchange rates, are shown as a two-way quote: buyer's margin and seller's margin. Since the buy rate (regardless of spot or forward) must always be lower than the ask rate (and the margin between the forward bid and offer rates must be greater than the margin between the spot bid and ask rates), in the case of a discount a large figure is deducted from the purchase rate spot, and the smaller one - from the spot selling rate. In the case of a premium, on the contrary, a smaller figure is added to the spot buying rate, and a larger figure to the spot selling rate.

Margin on Forex

Bookmaker's margin

A bookmaker is a legal entity whose activity is to accept bets from its clients on various events. In case of a correctly predicted outcome, the player receives a win. If the bet is incorrect, the size of his bet goes to the office. The office's business plan provides for regular monitoring of public opinion on various events, and therefore, regardless of the outcome of the matches, the bookmaker always has a guaranteed profit. The size of this profit is called margin.

After registering with a bookmaker’s office, the player becomes available to a rich list of sporting events, the so-called “line”. The player's task is simple to choose the match he likes and correctly predict its outcome. And in the event of a correctly predicted outcome, the bookmaker replenishes the player’s account with the amount of winnings. But the probability of the outcome of an event, as is known, is not the same.

About bookmaker margin

Each bookmaker has its own margin. The larger the office, the more extensive its list of client-players, the smaller the margin ensures a good profit. For large companies that have already earned a name in the world market and have a large turnover of funds, 5% is quite enough. In small offices, the margin ranges from 10% to 20%, which affects the attractiveness of the odds.

Bank margin

Bank margin is the difference between credit and deposit interest rates, between credit rates for individual borrowers, between interest rates on active and passive transactions.

Interest margin

Interest margin is the difference between interest income and expenses of a commercial bank, between interest received and paid. It is the main source of bank profit and is designed to cover taxes, losses from speculative transactions and the so-called “burden” - the excess of non-interest income over non-interest expenses, as well as banking risks.

The size of the margin can be characterized by its absolute value in rubles and a number of financial ratios.

The absolute value of the margin can be calculated as the difference between the total interest income and expense of the bank, as well as between interest income on certain types of active operations and interest expense associated with the resources used for these operations. For example, between interest payments on loans and interest expense on credit resources.

The dynamics of the absolute value of the interest margin is determined by several factors:

The volume of credit investments and other active operations generating interest income;

Interest rate on active bank operations;

Interest rate on passive bank operations;

The difference between interest rates on active and passive operations (spread);

Share of interest-free loans in the bank’s loan portfolio;

Shares of risky active operations that generate interest income;

The ratio between equity capital and attracted resources;

The structure of attracted resources;

The method of calculating and collecting interest;

System of formation and accounting of income and expenses;

Inflation rate.

There are differences between domestic and foreign standards for accounting for interest income and bank expenses, which affect the size of the interest margin.

There are two methods of accounting for transactions related to the attribution of accrued interest on attracted and placed funds to the bank’s expense and income accounts: the cash method and the “accrual” (“accumulation”) method.

Net interest margin (NIM) is one of the key performance indicators of a bank, reflecting the effectiveness of active operations carried out by the bank. Defined as the ratio of the difference between interest (commission) income and interest (commission) expenses to the bank's assets.

Bank profitabilityLending margin

Lending margin is the difference between the cost of the bank's borrowed funds and income from lending.

Credit margin

It's no secret that banks do not issue loans to their clients at cost. Banks increase the interest rate by a certain amount of percentage depending on the degree of risk. This difference between the cost of the goods, according to the loan agreement, and the amount of the loan for the purchase of goods, is called the loan margin. Among all credit products, the highest credit margin is in card lending, slightly lower in POS lending (so-called store loans), and even lower in consumer lending (loans issued in cash). Lowest loan margins in mortgage lending and auto lending.

According to existing financial law, the high risk associated with the provision of a loan must correspond to the high profitability of the operation (risk premium) and vice versa. Therefore, loans issued against liquid collateral (mortgages, car loans) are less risky and bring the bank less income than consumer lending or card loans. The largest credit margin is in card lending, since it is the most risky; in fact, funds are lent against the borrower's turnover on the account without any collateral. The margin in such lending can be more than 10%. Approximately the same loan margin is included by banks in the cost of the loan when applying for consumer loans. This is due to the fact that loans are provided without collateral, which means they are the most risky for the bank. Today, many banks that are actively involved in providing card and consumer loans have losses alone reaching 15-20%, so risks are built into the credit margin.

Recently, banks have slightly reduced the number of loans issued in cash, reduced margins, and accordingly lowered rates. In return, the prospective borrowers received requirements for additional security for loan repayment: life insurance, guarantee of one or two persons, mandatory employment. Both the first and second reduce banking risks, hence margins and rates. Now the undisputed leaders in terms of cost are card loans. As for mortgage loans, the margin on them is a few percent per annum, since they are less risky, the risk is almost zero. In car loans, risk is reduced by collateral.

Car loans and mortgages have the lowest interest rates: in car loans about 13%, in mortgage lending - 14%, in consumer lending - 21-25%. It is worth noting that not all profits go into the bankers' pockets. The margin should not be confused with the income that the bank receives from providing a loan, because due to large risks and losses, the income may be small and the margin may be high. The margin includes not only income, but also expenses, losses, mandatory reserves and the cost of liabilities. Different types of lending use different sources of liabilities, which also have different levels of risk, so the level of income is approximately the same even at different rates.

Solvency margin

Solvency margin is indicator of the solvency of an insurance company. It is calculated as the difference between the insurer's assets and its liabilities.

Assessing and monitoring the solvency of an insurance company is important for each insurance organization and for the entire insurance market. Insurance supervisory authorities develop solvency requirements and establish restrictive measures for those insurance organizations that do not meet these requirements. One of the requirements for insurance organizations is to establish a minimum level of solvency margin, which is determined through the standard ratio of assets and liabilities of the insurer.

The standard ratio between the assets and liabilities of the insurer is understood as the value (solvency margin) within which the insurer must have equity capital free from any future obligations, with the exception of the claims of the founders, reduced by the value of intangible assets and receivables whose repayment terms have expired.

The Regulations on the procedure for calculating by insurers the standard ratio of assets and insurance liabilities accepted by them, developed and approved by the Ministry of Finance of the Russian Federation, establishes a methodology for calculating the solvency margin. Insurance companies, in accordance with this Regulation, based on accounting and reporting data, analyze their financial position every quarter, including calculating the solvency margin.

Control of the solvency margin comes down to calculating the standard solvency margin and the actual solvency margin. An insurance organization is considered to meet solvency requirements if the actual solvency margin is greater than or equal to the standard solvency margin.

Dumping margin

Dumping margin - in foreign trade activities, the ratio of the normal value of a product (the price of a similar or directly competing product in the state of the manufacturer or exporter (union of foreign states) of the product in the normal course of trade in such a product, minus the export price of such a product to its export price. In accordance with the Federal Law " On measures to protect the economic interests of the Russian Federation in foreign trade in goods” (Article 8), the dumping margin is determined based on a comparison of the normal value of the product that is the subject of an anti-dumping investigation in the exporter’s country and the export price of the specified product. The dumping margin is considered to be the minimum acceptable. 2%.

Sources and links

Sources of texts, pictures and videos

wikipedia.org - free encyclopedia Wikipedia

bizkiev.com - electronic magazine about business

marketch.ru - information site about marketing

finansiko.ru - website about finances and earnings

dic.academic.ru - dictionaries and encyclopedias on Academician

prostobiz.ua - information site about business and finance

offisny.ru - information site to help merchants

s-tigers.com.ua - site about trading and management

ru.bforex.com - site about trading on the Forex market

probukmeker.ru - site about bookmakers and bets

interactivebrokers.com - site about stock trading

emagnat.ru - magazine about business and finance

signaliforex.ru - site about trading on the foreign exchange market

forexarena.ru - site about trading on the Forex market

zhuk.net - website about company management

btimes.ru - magazine about business in Russia and abroad

banki.ru - site about banks and banking

banki-delo.ru - site about banks and finance Banking

programma-avtokreditovaniya.ru - information site about car loans

vedomosti.ru - Vedomosti information and news portal

finances-analysis.ru - site about financial analysis

moneytimes.ru - online magazine about finance

ngpedia.ru - electronic encyclopedia of oil and gas

iknowit.ru - online magazine How things work

futures101.ru - blog about futures and derivatives market

allfi.biz - information portal about investments

aup.ru - administrative and management portal

pravoteka.ru - legal assistance portal Pravoteka

mrcmarkets.ru - site about forex trading

macd.ru - website about finance and stock quotes

afdanalyse.ru - site about methods of financial analysis

lawmix.ru - information site about business

msfo-dipifr.ru - site about IFRS and the Dilifr exam

Links to Internet services

forexaw.com - information and analytical portal on financial markets

google.ru - the largest search engine in the world

video.google.com - search for videos on the Internet using Google

translate.google.ru - translator from the Google search engine

yandex.ru is the largest search engine in Russia

wordstat.yandex.ru - a service from Yandex that allows you to analyze search queries

video.yandex.ru - search for videos on the Internet via Yandex

images.yandex.ru - image search through the Yandex service

Application links

windows.microsoft.com - website of Microsoft Corporation, which created the Windows OS

office.microsoft.com - website of the corporation that created Microsoft Office

chrome.google.ru - a frequently used browser for working with websites

hyperionics.com - website of the creators of the HyperSnap screenshot program

getpaint.net - free software for working with images

etxt.ru - website of the creators of the eTXT Anti-plagiarism program

Article creator

vk.com/panyt2008 - VKontakte profile

odnoklassniki.ru/profile513850852201- profile in Odnoklassniki

facebook.com/profile.php?id=1849770813- Facebook profile

twitter.com/Kollega7 - Twitter profile

plus.google.com/u/0/ - profile on Google+

livejournal.com/profile?userid=72084588&t=I - blog on LiveJournal

Margin: what is it in simple words? Types of margin

The term “margin” is heard by every person associated with business. Often, beginning businessmen and ordinary people confuse margin with profit, considering one word to be a substitute for the other. However, despite the fact that both concepts help to evaluate the economic result of an organization’s activities, there is still a difference between them. Let's try to figure it out.

The meaning of the word “margin” in different areas:

- Margin(in a professional sense) - collateral for obtaining a loan in monetary or commodity equivalent, which is subsequently used to carry out a speculative stock exchange transaction;

- Margin(translation from English - difference; advantage) - a coefficient used in economics that denotes the differences between financial quantities. For example, stock prices or product prices;

- In general market vocabulary, the difference between the price of a product or service and its cost (analogy with profit).

Abroad, margin is considered an interest rate that determines the proportion of profit to the final price of the product. Thus, the progressiveness of a particular company is assessed. In our country, margin means “net profit”, so there is no talk about special computational methods for determining margin or profit, due to the fact that they are practically the same thing.

What are the margins?

- Operating margin – the ratio of a company’s operating revenue to its income. Simply put, it shows how much money a company makes or loses from its core business for each unit sold;

- Gross Margin – percentage of gross profit from each ruble of sales. As this percentage increases, the premium that the company will receive after selling goods and services also increases;

- Variation margin a is the amount that is paid or deducted from the trader’s cash balance based on the results of the configuration of currency obligations during transactions. Also, this is an indicator by which the amount of funds taken as collateral may increase or decrease. The margin level varies depending on the trading results: at the end of the trading session, the accrued variation margin is added to the account or withdrawn from it (back margin). If a trader holds a position for one trading session, the trading result will be equal to the variation margin. If the trader remains at the same level for a long time, it will continue to increase every day, after which, ultimately, the VM indicators will be different from the monetary outcome of the transaction;